A surge in global derivatives trading in the first quarter of 2026 masked a more significant shift in how market participants are managing risk, with options increasingly favoured over futures as geopolitical uncertainty reshaped hedging strategies.

Data covering trading activity across more than 60 derivatives exchanges tracked by FIA showed record levels of activity as markets reacted to a volatile start to the year. One of the key themes explored in an FIA webinar earlier this month, hosted by Will Acworth, FIA’s global head of market intelligence, was how volume and open interest trends reflected the impact of the conflict in the Middle East on both commodity and financial futures and options markets.

Globally, exchange-traded derivatives volume rose to 38.35 billion contracts in the first quarter, up 38.8% year-on-year. Options accounted for most of the activity, with volumes increasing 39.7% to 28.61 billion contracts, compared with a 36.3% rise in futures to 9.74 billion.

Open interest – the total number of outstanding contracts that have not been settled – reinforces that trend. By the end of March, options open interest had risen 20.2% year-on-year to 1.25 billion contracts, outpacing the 17.0% increase in futures open interest, which reached 371.8 million contracts. In total, open interest across futures and options rose 19.4% to 1.62 billion contracts.

Behavioural shift

Beneath those headline figures, the data points to a shift in behaviour. Acworth pointed out a shift towards using options for hedging rather than futures as one of the more persistent trends in exchange-traded derivatives markets. While options typically involve an upfront premium, they can offer greater certainty over downside or upside exposure. And for buyers, options help them avoid the variation margin calls associated with futures during periods of sharp market moves.

That distinction is becoming more relevant in markets shaped by geopolitical shocks. In gas oil, a key European fuel benchmark, futures trading volume surged but open interest grew only modestly, suggesting activity was driven more by short-term positioning than by longer-term hedging.

By contrast, options activity points to a greater build-up of hedging positions. Options on gas oil have seen rapid growth in both trading activity and open interest, reaching record levels. “This is not a market where you’re seeing a lot of retail punters,” Acworth noted. “This is an institutional market… and it reflects a change in behaviour among hedgers in how they want to cover their risks.”

The same divergence is evident in crude oil. As markets assessed the potential disruption linked to the Strait of Hormuz, trading volumes in ICE Brent futures rose sharply, while open interest declined. Options open interest, however, increased. “We are in a very uncertain environment,” Acworth said. “Options actually provide a very cost-effective way to hedge when you really have no idea what the outcome might be.”

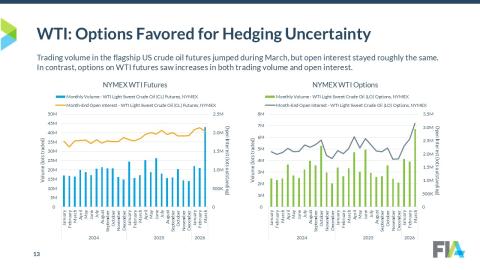

Even in markets less directly exposed to the conflict, similar dynamics were evident. Options on West Texas Intermediate crude oil listed on the New York Mercantile Exchange also saw a marked increase in open interest, suggesting that participants are hedging against uncertainty over the duration and broader impact of the disruption.

Data from individual exchanges reinforces the trend. At the London Metal Exchange, options reached an average daily volume of 66,611 lots in the first quarter, up 138.9% year-on-year. Open interest in options and TAPOs [traded average price options] increased by 52.5%, compared with a 2.6% rise in futures open interest.

Short-dated contracts

The shift is not confined to commodities. In US equity markets, options activity has expanded alongside the growth of short-dated contracts. Exchanges now offer expiries across the week, allowing traders to target more specific windows of risk, driving demand for products such as S&P 500 index options.

A similar pattern is emerging in interest rate markets, where uncertainty over monetary policy has increased demand for more flexible hedging tools. “If rates could go up or down and there’s a 50/50 chance of either, use options,” said Josh Cannington, vice president of interest rate derivatives at StoneX. “That flexibility is becoming more important as companies reassess how they manage exposure in a less predictable environment.”

The growing use of short-dated options underscores the shift. Researchers at CME Group say these instruments are increasingly used to manage event-driven risk. In a recent analysis, Gregor Spilker and Emily Balsamo noted that “in a period defined by rapid news cycles… monthly expiry schedules often need to be complemented by managing event-specific risks,” with weekly contracts allowing participants to “isolate specific windows of volatility, such as central bank announcements or geopolitical developments, without incurring the time-value premium of longer-dated options.”

Taken together, the data suggests that options are playing a more central role in risk management.

Futures remain essential for liquidity and price discovery. But in an environment defined by geopolitical disruption and policy uncertainty, options are increasingly being used to fine-tune exposure.

For many market participants, the shift marks a move away from broad, directional hedging towards more precise strategies that respond not just to where markets are heading, but to how uncertain that path has become.