Retail investors fuelled a sharp rise in trading activity across precious metals derivatives in 2025, while institutional benchmark futures contracts saw comparatively muted growth, according to data presented on an FIA ETD Trends webinar earlier this month.

Trading volumes in smaller-sized gold futures and exchange-traded fund options expanded rapidly, particularly in the US, reflecting growing participation from individual investors, said Will Acworth, FIA's global head of market intelligence.

“The big takeaway is we saw tremendous growth in trading volume of contracts that I would describe as primarily retail,” Acworth said. “Not such large growth in the more institutional contracts.”

Options on precious metals ETFs traded in the US posted especially strong gains in both volume and open interest, he said. By contrast, activity in benchmark gold futures listed on COMEX, a subsidiary of CME Group, showed little change over the same period.

The divergence underscores what Acworth described as one of 2025's defining themes: a wave of retail-driven participation in commodity derivatives.

Exchanges have moved quickly to meet that demand, he added. CME now offers gold futures in four sizes – 100 ounces, 50 ounces, 10 ounces and 1 ounce – broadening access for retail investors. The exchange also plans to launch a smaller-sized silver futures contract, Acworth noted.

Gains after dark

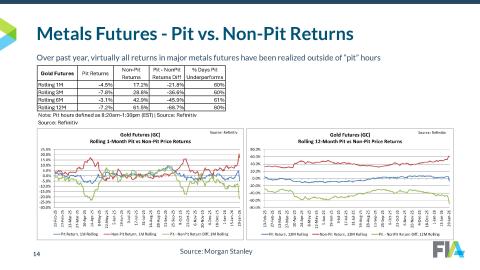

A shift in trading patterns has also been evident in the timing of returns, said Erin Perzov, head of quantitative futures content at Morgan Stanley.

Using intraday data across futures markets, Perzov analysed returns during traditional “pit” hours – the legacy daytime trading window – versus “non-pit” or overnight hours. Although physical trading pits have largely disappeared, many futures contracts still maintain defined daytime sessions that serve as reference points for liquidity and pricing.

Over the past year, the bulk of gains in US precious metals futures have occurred outside those traditional daytime windows, Perzov said.

In gold futures, virtually all returns were generated during non-pit hours. Investors holding COMEX gold futures long only during pit hours over the past year would have lost about 7%, she said. By contrast, those holding positions exclusively during non-pit hours would have gained roughly 61%.

“Almost all of the returns – and in this case, all of the gain – has happened outside of traditional pit trading hours,” Perzov said.

The webinar discussion highlighted a similar pattern in other metals, such as silver and copper. In COMEX copper futures, being long during pit hours would have produced little return over the past year, while gains of around 31% were realised entirely during non-pit trading hours, Perzov said.

The trend holds across multiple rolling time horizons, including one-month and 12-month periods, and stands out relative to 25 years of historical data analysed by Morgan Stanley.

Price discovery

The concentration of returns in overnight trading raises questions about where price discovery is taking place. Because the overnight window overlaps with European and Asian trading hours, the data may point to a greater role for non-US participants in driving price moves. Metals have long traded on global macro themes – including currency shifts, central bank policy and geopolitical risk – and electronic trading has blurred geographic boundaries.

“Are these returns coming outside of US hours from traders outside of the US, for example?" Perzov said. “I think this is broadly consistent with the point around a lot of the activity coming outside of these traditional US institutional contracts.”

At the same time, the industry has not found consensus on whether more asset classes should move toward continuous, 24/7 trading, a structure already common in cryptocurrencies.

While precious metals futures do not yet trade on a fully continuous basis, the widening dispersion between daytime and overnight returns suggests that activity outside traditional US hours is increasingly influential.

For exchanges and clearinghouses, the trends underscore the importance of product design, margining and operational readiness in a market where participation is broadening and price action increasingly unfolds beyond historic trading hours.

View the Trends in ETD Trading: Year in Review webinar and related slides here.