The global shift to renewable power is spurring the creation of new infrastructure – and not just wind farms, solar plants, battery storage and transmission lines. Financial tools are also playing a role by helping buyers and sellers of renewable energy manage their price risk.

One example is a recently announced alliance between the European Energy Exchange, Europe’s leading wholesale power market, and Pexapark, a software and advisory company based in Zurich that specializes in working with the renewables industry.

Pexapark's clients include European power companies such as RWE and Vattenfall as well as renewable players such as Vestas, the Danish wind turbine manufacturer. It provides them with analytical tools for calculating the risks involved in building renewable energy projects and selling the output on the open market.

The partnership between EEX and Pexapark is aimed at the opportunity created by the collision between two major trends: a rapid increase in the amount of power produced from renewable sources such as solar and wind, and a decline in government subsidies for renewable power producers. That makes the price of renewable power much more volatile and creates an opportunity for the derivatives industry to step in and offer market-based instruments for managing price risk.

Coping with uncertainty

In the past, government subsidies meant that renewable power producers faced very little price risk.

"You constructed it, you knew the cost, and then you knew pretty much accurately, only subject to production fluctuation, what kind of money you were going to get out of it,” explained Werner Trabesinger, head of quantitative products at Pexapark. "But now in many European geographies, these subsidies are being phased out."

Power buyers and sellers now face enormous price swings of as much as 30% on any given day, according to Trabesinger. The volatility stems from the fact that most renewable power sources do not behave like conventional fossil fuel plants.

"If historically you had gas plants, you’d trade the peak hours, because you’d more likely run them from 8 in the morning to 8 in the evening. The challenge you have with renewables is intermittent generation. Either you have a [photovoltaic] plant and then basically you get concentrated production in a few hours of the day, or you have wind where it’s pretty random."

Such fluctuations make it difficult to finance construction of new renewable power infrastructure without a long-term contract with a utility, according to Trabesinger. "With 15-30% volatility, no bank on earth is going to fund you if you just take your production to the spot market," he said.

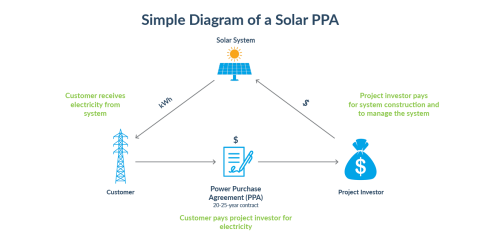

Enter the Purchase Power Agreement, an increasingly popular long-term contract that gives the power producer the price stability it needs to operate. PPAs are often used by developers of solar systems and wind farms to lock in the sale of power at a fixed rate over the next 10-25 years. With the sale of the output assured, it becomes much easier for the developer to find funding for the construction of the project.

The popularity of PPAs has grown dramatically worldwide in recent years. Bloomberg estimates that corporate purchases of such contracts grew from 13.6 gigawatts in 2018 to 23.7 gigawatts in 2020, a 43% gain. The US is currently the largest PPA market overall, but Europe has the lead in the use of PPAs for renewable power, with 45% of all renewable power produced in Europe, the Middle East and Africa contracted under a PPA, according to Bloomberg.

Better insights into pricing

Pexapark and EEX are hoping to encourage European power producers and buyers to set up more PPAs by improving transparency into the pricing dimension of these agreements. The Leipzig exchange is contributing its price data to PexaQuote, the Swiss firm's PPA price reference platform, starting with German power futures, the most heavily traded contract in its power futures complex.

Trabesinger said that the addition of these data gives power producers a better sense of the current value of their contracts. It also helps Pexapark’s analysts plot estimates of energy prices up to two years ahead. Pexapark uses those inputs to run 10-year Monte Carlo price simulations, enabling analysts to generate a price estimate that has a 90% break-even probability. Other analytics firms can generate a fair value price, but without the same insight into volatility.

"That’s our secret sauce, if you will," said Trabesinger. "Most everyone manages to work out the fair value, but [calculating] how large these risk adjustments should be requires simulation – a lot of calibration to volatility and whatnot – and that's what most people cannot do," he said.

The seller’s risks are eliminated once the PPA is signed, but not the buyers. Buyers typically hedge 70% of the value for the first year and 30% for the second – a two-year horizon that Trabesinger believes is a convention inherited from thermal power trading. "Once that is in place, what you do is you just roll it forward year on year for the entire 10 years," he explained.

To support the long-term planning that goes into the financing of this new infrastructure, EEX is working to extend the dates covered by its power futures. Viviana Ciancibello, senior business developer for European power derivatives at EEX, said that the exchange is now planning on stretching its power futures contracts to 10 years in Spain, Germany, and Italy.

"EEX believes that 10-year power futures are a key enabler of future renewable energy growth in Europe, since counterparties will be able to effectively offload risk onto our clearinghouse," Ciancibello said.

Learning to hedge

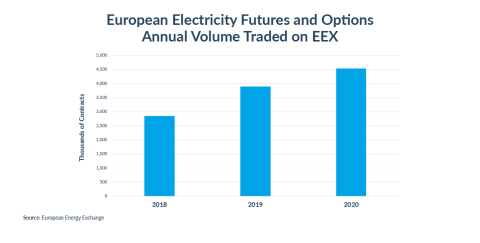

Although about 50% of European power is now traded through EEX, many renewable players have not learned to work with futures.

One reason, according to Trabesinger, is that many of the players lack experience. "You need to understand, obviously, how you work out the P&L of futures contracts. That’s new to a lot of them. And you need to understand cashflow implications because you’re going to have margin movements which you need to be prepared to meet. So there’s a whole education process to get them there," he said.

For now, renewable power traders in Europe are in the early stages of learning about using futures for risk management, according to Trabesinger. "At this point only the most sophisticated among them [hedge their power risk], but we are firmly convinced that going forward it will become something for more and more of them."

"The longer-run goal of this collaboration is essentially to inform our customers of the fact that electricity futures, as offered for example by EEX, are a good means of managing renewables risk," he said.

EEX extends maturities with an eye on renewable PPAs

The European Energy Exchange currently offers more than 100 futures and options contracts based on electricity prices in 20 power markets across Europe, including Germany, France, Hungary, Italy and Spain.

On 27 September, the exchange will extend the tradable yearly maturities for German, Italian and Spanish power futures to 10 years. EEX said this expansion will allow end-users to hedge price exposures up to 10 years in advance, and pointed in particular to the benefits for financing renewable power production through long-term purchase agreements.

"Many customers, especially in markets with widespread use of PPAs such as Spain, want to use the EEX futures for an even longer period of time to hedge their price and counterparty risk," Peter Reitz, the chief executive officer of EEX, said in a statement.

By adding these new maturities EEX is providing additional instruments for the renewable energy sector which support the expansion goals of renewable energies and the transition from feed-in tariffs to subsidy free power markets," he added. "We’re convinced that such a market-based approach is a key element to successfully handle the challenges towards a decarbonised energy sector and a climate neutral economy."