Customer funds held at US futures brokers climbed to a record $442.7 billion in February 2026, according to the latest FIA analysis based on US government data published on 14 April. The figure is up 6% month-on-month and 26% year-on-year.

The data comes from the Commodity Futures Trading Commission, which requires all futures commission merchants – the term used for futures brokers in the US – to report the amount of customer funds they are holding.

Another key statistic published by the CFTC is the number of FCMs holding customer funds in futures accounts. That number edged higher to 52 firms in February, compared with 49 a year ago and 50 five years ago, underscoring a slow but steady broadening of the clearing landscape.

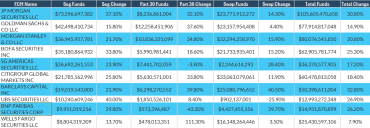

JP Morgan and UBS lead growth

The growth in customer funds was led by the largest clearing firms, with several of the top 10 FCMs posting strong double-digit gains.

JP Morgan Securities remained the largest holder of customer segregated futures funds, with $74 billion, up 37% year-on-year. UBS Securities saw notable expansion, with customer funds up 40% to around $10.2 billion over the same period.

Bank of America Securities, Morgan Stanley and other major bank FCMs also recorded solid increases, reflecting broad-based growth across institutional clearing activity.

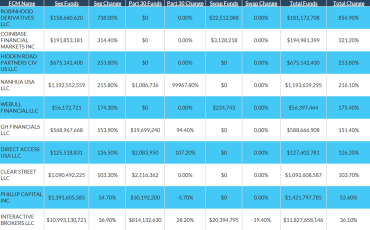

Retail participation

While large bank FCMs dominate in absolute terms, the most dramatic percentage growth came from non-bank and retail-focused firms.

Robinhood Derivatives, the futures arm of the popular digital brokerage firm, saw customer funds surge 738% year-on-year, albeit from a smaller base, reaching approximately $159 million. Coinbase Financial Markets also posted strong gains, alongside other retail-oriented and high-growth intermediaries, reflecting a sustained rise in retail participation in futures markets.

Clearing demand

The surge in customer funds reflects the heightened volatility across global markets, driven by geopolitical developments, shifting trade policy and rapidly changing monetary policy expectations.

Will Acworth, FIA’s global head of market intelligence, said the key driver has been a rise in volatility beginning in early 2025, triggered by a shift in US trade policy.

He noted that the inflection point in customer funds coincided with the US administration’s reorientation of global economic relations in early April 2025, often referred to as “Liberation Day.”

Volatility has increased since then following successive geopolitical shocks, including developments involving Venezuela and Iran, he commented. Those shocks have broadened market turbulence beyond commodities into interest rate markets through shifting inflation and policy expectations.

Whiplash

One of the clearest illustrations of market volatility has been the rapid repricing of US interest rate expectations, as reflected in the Fed funds futures curve.

Acworth described the moves as a “whiplash effect,” with expectations swinging sharply between cuts, hikes and pauses over a matter of weeks, forcing market participants to adjust positions quickly and contributing to elevated trading activity.

“You're seeing expectations for Fed policy change dramatically over just three weeks,” he said. “The fact that you would see such a dramatic change gives you a sense of why there would be so much trading, because market participants have to shift their positions.”

Source: CME Group, 1 April

A second major driver of rising FCM balances has been the expansion of retail trading activity in futures markets. Retail-focused firms recorded the fastest growth in customer funds over the past year.

Acworth noted that while percentage gains are amplified by starting levels, the trend remains significant. “It does show that retail participation is increasing dramatically,” he said.

Outlook

The data reflects conditions as of February 2026. However, given the escalation in geopolitical tensions and continued uncertainty around monetary policy since February, customer fund levels could see further gains in the coming months, potentially extending the current cycle of record balances and elevated derivatives activity.