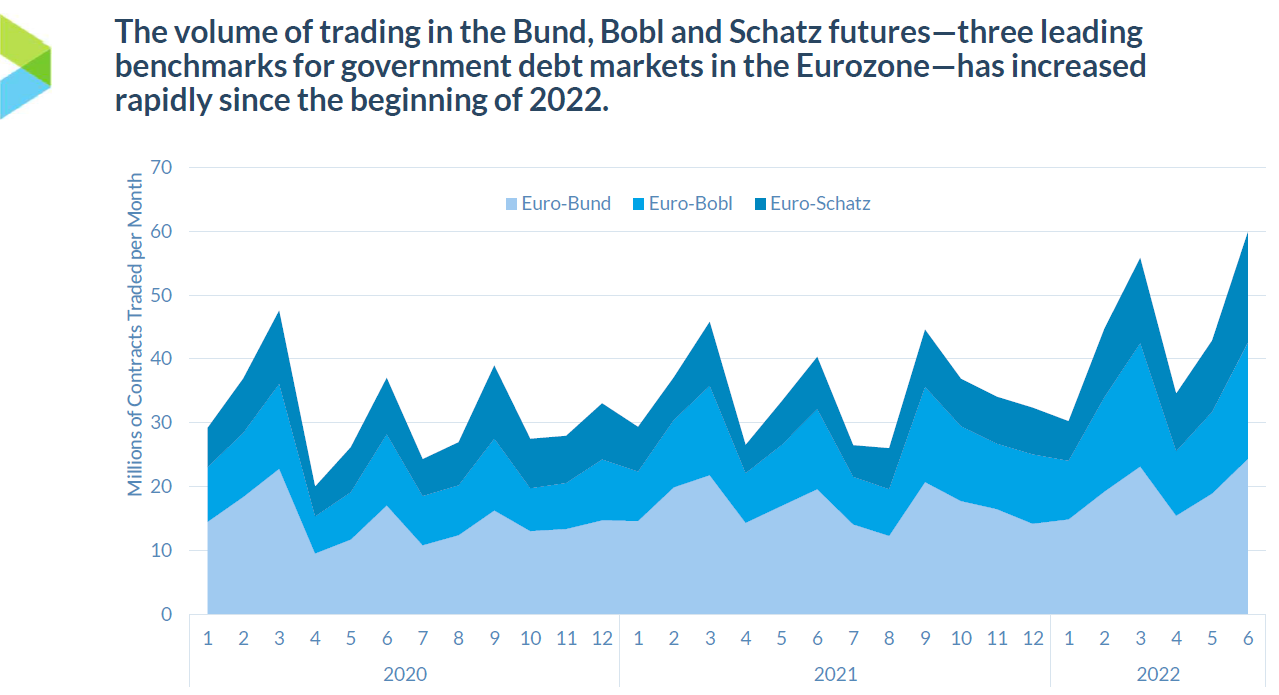

The interest rate complex at Eurex had a surge of activity in the first half of the year, according to data on trading volume and open interest. Futures on the Bund, Bobl and Schatz, three leading benchmarks for government debt markets in the Eurozone, all saw increases in activity over the previous year as market participants adjusted to changes in macroeconomic conditions as well as Russia’s invasion of Ukraine.

The Schatz futures in particular had a very sharp increase in trading activity. The number of contracts traded reached 13.3 million contracts in March, the highest in at least four years. Then in June, volume jumped to 17.3 million contracts, the highest ever for this contract.

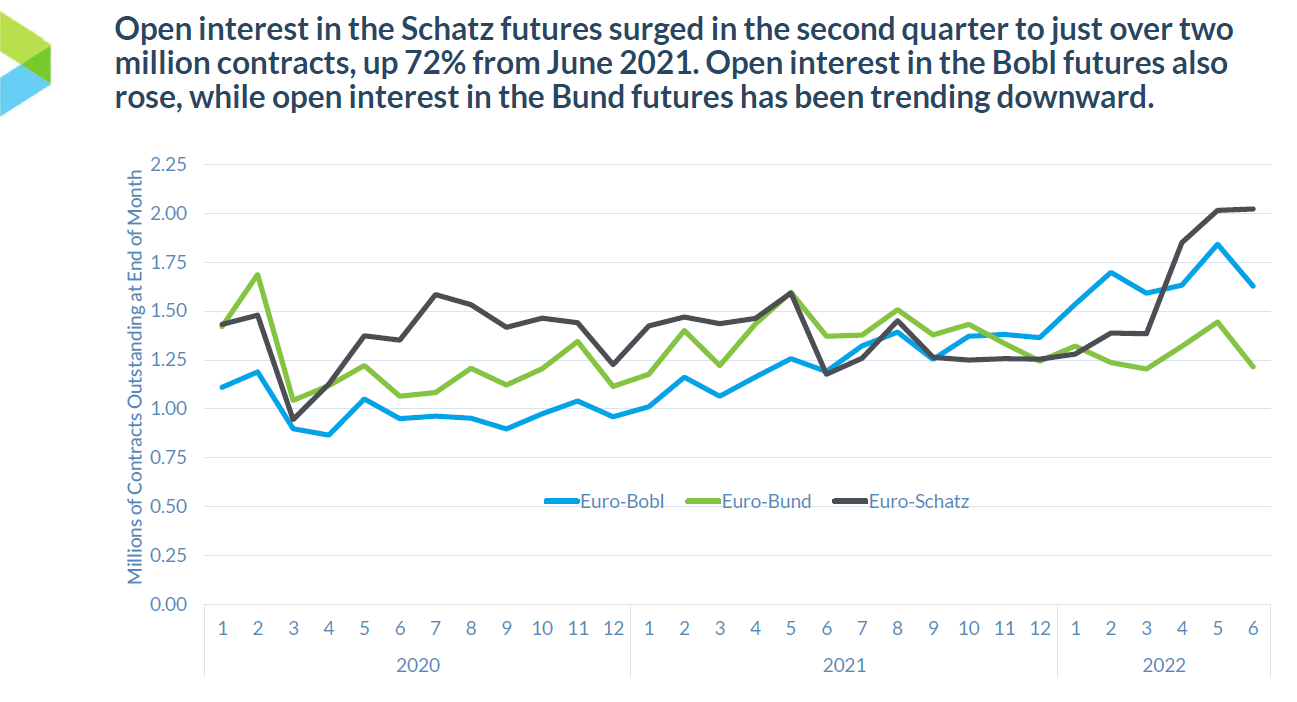

Open interest, which measures the number of outstanding positions, also picked up dramatically in the first half of the year. Open interest in the Schatz futures went from 1.25 million contracts at the end of 2021 to just over two million in June. In fact, open interest in the Schatz futures is now higher than any other interest rate futures at Eurex, including the Bund and Bobl futures (see chart below).

Schatz futures are based on short-term debt issued by the German government and serve as the benchmark for the two-year point on the interest rate curve. The Schatz futures, like the rest of the interest rate complex at Eurex, has been the focus of rapidly changing expectations for European economic growth and interest rate policy.

At the beginning of the year, the European central bank pivoted from promoting growth to fighting inflation. The central bank began reversing its quantitative easing program in March and signaled that a series of interest rate hikes would start in July. At the same time, the turmoil created by the Ukraine invasion, combined with the shock to commodity prices, created even more uncertainty about the near-term and medium-term outlook for economic growth and interest rates in Europe.

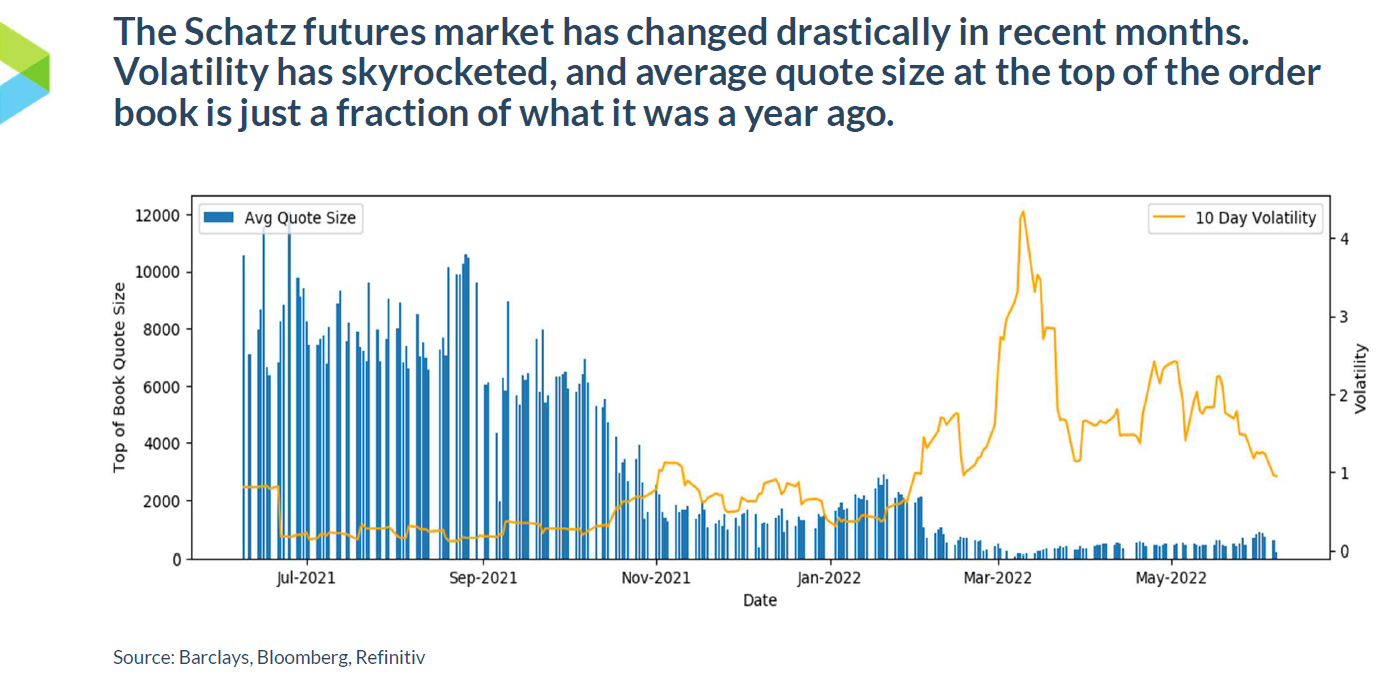

As a result, interest rate volatility has skyrocketed. According to Barclays, volatility for the Bund, Bobl and Schatz futures are all far above the levels a year ago. In a recent webinar hosted by FIA, Nick Ashwin from the electronic execution team at Barclays, presented some data on the level of volatility in these three interest rate futures as well as other interest rate futures listed on Eurex.

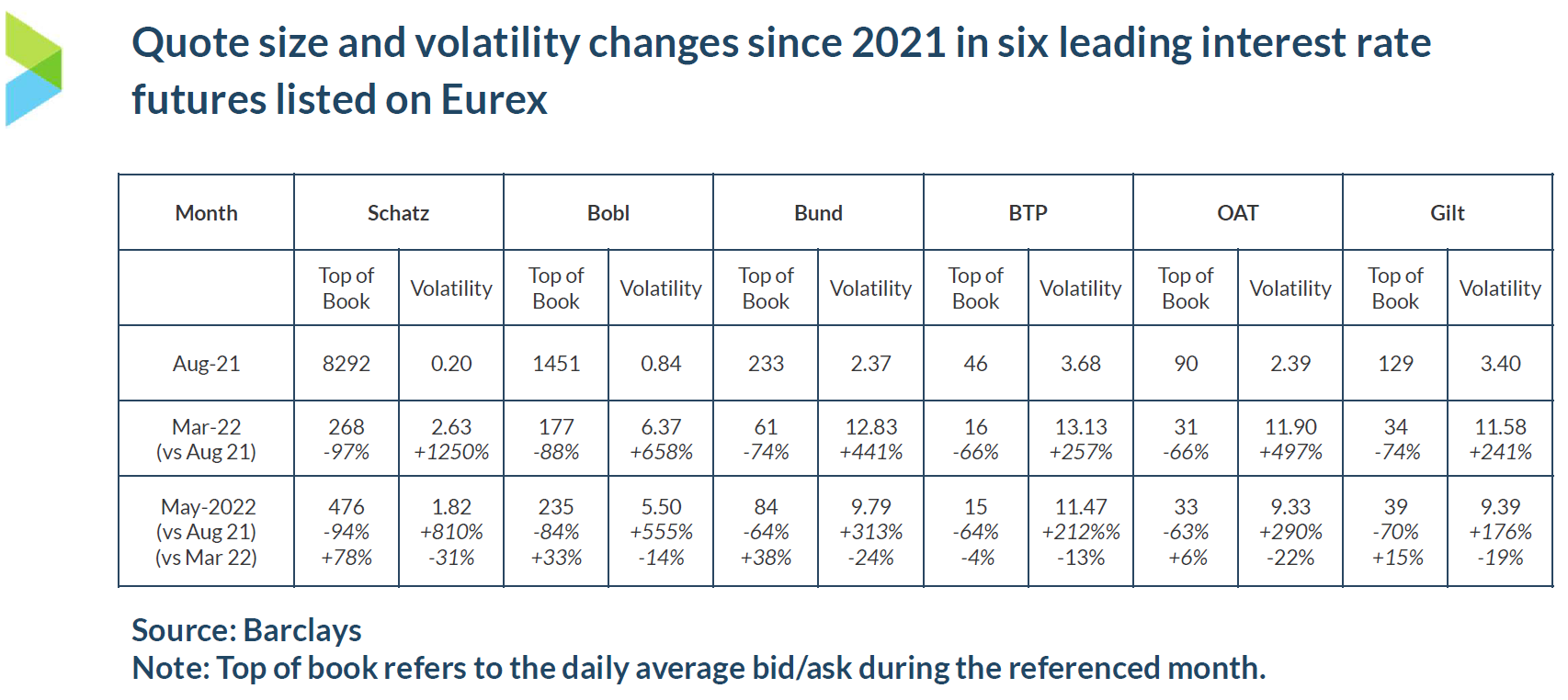

Ashwin commented that volatility for the Schatz futures reached a peak in March then came back in over the next several months, but remains far above the year-ago level. In addition, the change in the level of volatility from last year to this year was much more extreme than any of these other contracts. At the peak in March, volatility in the Schatz futures was 1250% higher than August 2021.

Equally important, the liquidity in these contracts has fallen significantly. During the webinar, Ashwin provided some estimates of top-of-book liquidity, i.e., average daily bid/ask size displayed in the Eurex order book. In the Schatz futures market, the top of book liquidity dropped from more than 8000 contracts in August 2021 to just 268 in March and 476 in June.

The Bund and Bobl futures also saw a sharp decline in displayed liquidity, although not quite as extreme. In the Bund futures market, Ashwin estimated that top of book liquidity fell from 233 contracts in August to 61 in March and 84 in June. In the Bobl futures, top of book liquidity fell from 1451 contracts to 177 and 235.

As a general rule, the amount of liquidity displayed in exchange order books tends to be inversely related to volatility, especially at the top of the order book. That is because the market makers that display bids and asks are wary of taking on too much risk when prices make a rapid move. Large amounts of trading can still move through the market—as shown by the large increase in trading volume in the Eurex contracts—but spreads between bids and asks tend to be wider.