The US Commodity Futures Trading Commission held a meeting of its Market Risk Advisory Committee (MRAC) on July 21 via teleconference.

The meeting covered a wide range of topics including the impact of the pandemic on derivatives markets, the current status of the transition away from the Libor benchmark, and an upcoming report on climate-related financial risks. The meeting featured presentations from representatives of trading venues, clearing firms, and central counterparties as well as comments from buyside firms such as Blackrock and Vanguard.

In addition, CFTC Chairman Heath Tarbert announced that the CFTC has completed "a detailed forensic study of the West Texas Intermediate crude oil price aberration on April 20th that led to negative oil prices," which he plans to make public this fall. Also, CFTC Commissioner Rostin Behnam, who sponsors the MRAC, said he plans to put "diversity and inclusion" onto the discussion agenda for the next meeting, which is likely to take place in December.

Initial margin and CCP risk issues

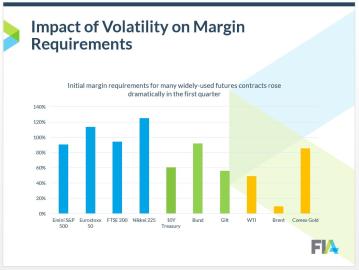

FIA Board member Alicia Crighton, co-chair of the MRAC's CCP Risk and Governance Subcommittee and global co-head of futures and head of OTC and prime clearing businesses at Goldman Sachs, represented FIA and its members at the MRAC meeting. She gave a presentation on how clearinghouses responded to market volatility in March, using FIA data to illustrate key points, and offered specific lessons learned by the significant changes in initial margin requirements.

- Crighton noted that US FCMs collected an additional $136 billion in collateral from their customers during the month of March. "That represents more margin for cleared customers than ever in the history of the CFTC, even more than the peak of the financial crisis in 2008," she said.

- Citing data from an FIA survey conducted in June, Crighton reported that 76% of market participants experienced operational disruptions because of margin volatility in March.

- Crighton acknowledged that "it is not unusual for CCPs to increase IM requirements during periods of market stress," but warned that "this is exactly the time you do not want to demand such dramatic increases in margin" because those historic increases compounded other industry challenges.

- The current clearing system is vulnerable to these "procyclical" effects of margin, Crighton said, and it is important for market participants to consider improvements to margin methodologies so that collateral requirements will neither "chase volatility down" nor spike as quickly when volatility rises.

Crighton also noted the stresses caused by how CCPs manage their end-of-day clearing cut-off times for settlement. She noted that "most CCPs were very accommodating and extended the clearing windows" but coordination and transparency should be improved across the marketplace.

Representing the clearinghouse perspective was Lee Betsill, subcommittee co-chair and the managing director and chief risk officer at CME. He noted that, like other firms, clearinghouses should be proud of their operational resilience during the pandemic as they took on new remote workflows amid record volumes but experienced no significant disruptions or downtime. Betsill also defended margin methodologies used by clearinghouses, noting that "the size of the overall IM increases relative to extraordinary volatility observed" was "relatively muted" given the extraordinary circumstances at the time.

Benchmark reform and CCP discounting transition

Thomas Wipf, chairman of the MRAC's Interest Rate Benchmark Reform Subcommittee and vice chairman of institutional securities at Morgan Stanley, discussed progress towards an orderly global transition away from LIBOR and other legacy interest rates by the end of 2021.

Wipf noted that US market participants held a "tabletop" exercise in June focused on CCP discounting transitions. The exercise included CME and LCH, the two leading CCPs for cleared interest rate swaps, as well as swap dealers and other market participants that will be affected when the two CCPs switch to SOFR-based discounting in October. He specifically highlighted concerns including:

- Gaps in understanding among market participants about precise timing of discounting transition milestones, as well as dynamics of CME and LCH auction processes

- Potential disruptions that may be caused by an auction where discounting risk swaps cannot be liquidated despite the end user’s election to offload these swaps

- A lack of consistency between CCP-mandated dates by which market participants must finalize elections to offload discounting risk swap compensation

- Major differences between CCP plans that could create significant operational and market risk for participants over the discounting transition period

To help mitigate these potential issues, the Interest Rate Benchmark Reform Subcommittee offered key considerations that include risk mitigation strategies such as trade compression and re-couponing by market participants as well as better industry education and proactive engagement by all stakeholders.

The Subcommittee's report on the LIBOR transition also included three recommendations that were adopted by the MRAC for consideration by the CFTC commissioners in future rulemakings:

- Consideration of the implications of real-time public reporting requirements for discounting risk swaps and concerns that these requirements may disincentivize bidding in the auctions.

- Consideration of relief from tax and accounting implications of pre-hedging auction related exposures

- Consideration of relief in the uncleared markets for swaptions and amendments to credit support annexes

Climate risk

The Climate-Related Market Risk Subcommittee said it anticipates the release of a comprehensive report on the issue "either in August or at the very beginning of September." No specifics were issued in advance of the final document. Bob Litterman, the subcommittee chairman and founding partner at Kepos Capital, expressed hope that the report will help to inform policy debates in the US Congress and state legislatures. He also urged US financial regulators including the CFTC and others to "recognize that climate change poses serious emerging risks to the US financial system” and “move urgently and decisively to better measure, understand, and address these risks."

Market structure and pandemic-related issues

Bloomberg and TradeWeb, the two largest dealer-to-client Swap Execution Facilities (SEFs) offered insights on the impact of the pandemic on market quality metrics for the swap market, such as liquidity, transaction numbers, and "hit" ratios for RFQ trades. They also affirmed that the OTC rates markets remained liquid throughout the crisis despite very high volatility and large increases in transactions. Clarus Financial added data showing that usage of clearing remained at very high levels for standardized OTC interest rate swaps during this period.

A different perspective was offered by several buyside representatives, led by Sam Priyadarshi, the global head of portfolio risk and derivatives at Vanguard. He noted that there was a short period when much of the fixed income markets became "dysfunctional" with limited liquidity available from dealers and very wide bid-ask spreads. He pointed in particular to what he called the "unraveling" of the futures basis, which tracks the spread between Treasury futures and cash Treasuries, that was caused by multiple simultaneous demands for liquidity. It was only after the Federal Reserve intervened with "extraordinary levels of balance sheet accommodation" for the banking system that these markets stabilized, he said.

The MRAC's Market Structure Subcommittee also noted that the recent market stress caused by the COVID-19 pandemic caused the subcommittee to redirect its efforts, but going forward it will return to normal priorities including recommendations on the swap dealer landscape and the Made Available to Trade (MAT) process.