CBOE moves into new markets with bats acquisition

In late September, CBOE Holdings, the parent company of the Chicago Board Options Exchange, and Bats Global Markets announced plans to merge in a deal valued at $3.2 billion. The transaction, expected to close during the first half of 2017, will have a number of important effects on the U.S. equity options market.

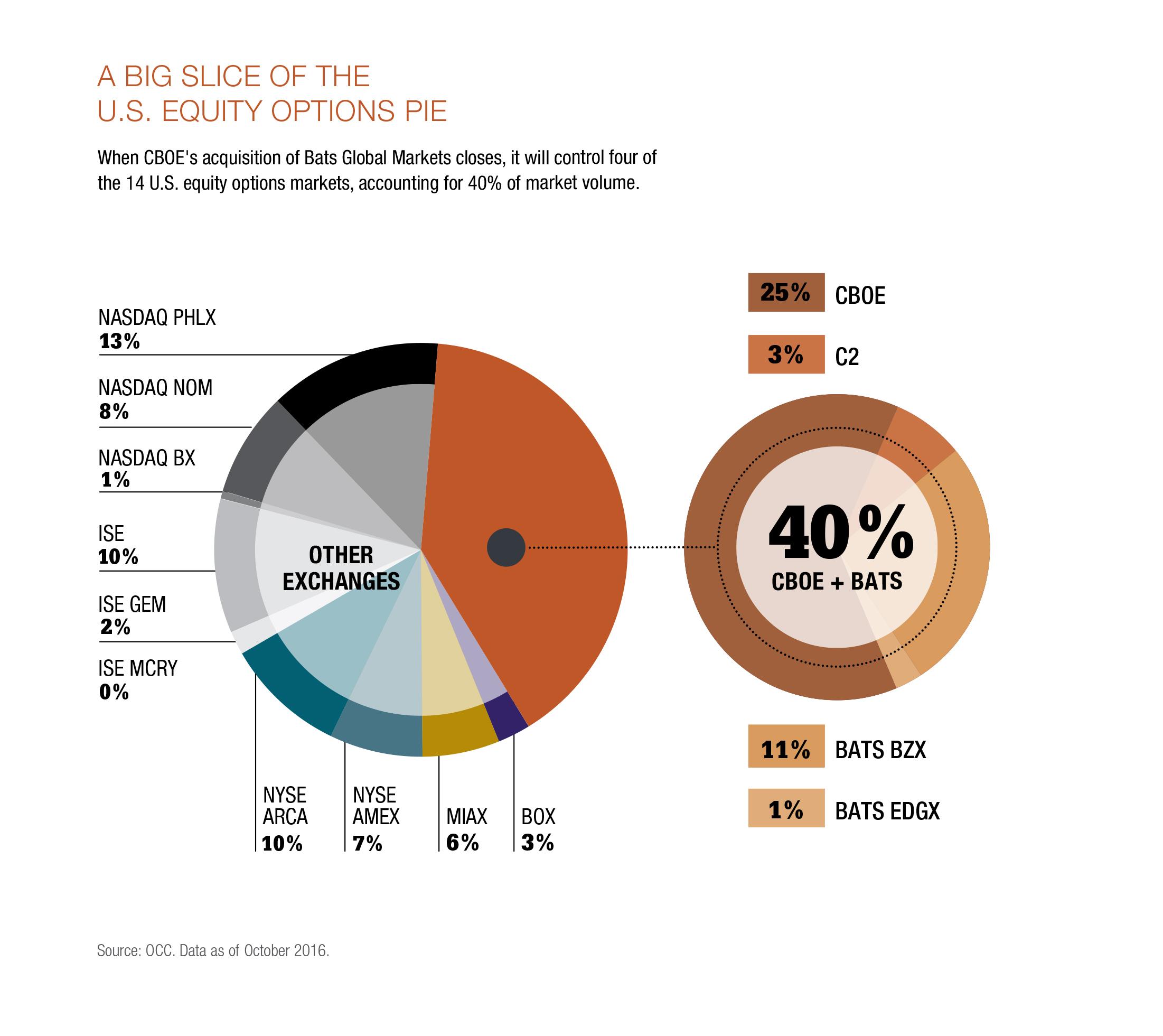

Most obviously, it will continue the consolidation trend put into motion earlier this year with Nasdaq's acquisition of the International Securities Exchange. Following this latest deal, three entities — Intercontinental Exchange's NYSE, Nasdaq and the combined CBOE-Bats — will control 85% of the trading in equity options.

Leading ASR systems use deep neural networks as the core technology to model the sounds of a to assess which sound a user is producing at every instant in time.

The combination of CBOE and Bats will be particularly important for the index side of the business. Bats is the leading U.S. marketplace for exchange-traded funds, which are increasingly emerging as the preferred vehicle for equity investing. Options on ETFs are the fastest growing segment in the equity options market and now account for 50% of total volume. Add in the CBOE's proprietary index products, and the combined exchange will have a commanding position on this side of the business.

For brokers and clearing firms, perhaps the most important implication of this deal is the potential consolidation in trading technology. Officials from the two exchanges have said that they plan to migrate CBOE's options exchanges—CBOE and C2—to the Bats platform, which is known for its speed and reliability. Bats has already migrated numerous other platforms including Chi-X and Direct Edge to its platform successfully.

In terms of trading volume, the combination of CBOE and Bats will give the company a 41% share of the U.S. equity options market. That compares to 34% for the six venues operated by Nasdaq and 17% for the two venues operated by NYSE (see "A Big Slice of the U.S. Equity Options Pie" below).

The merger will also have implications outside the U.S. Bats operates the largest equity exchange in Europe in terms of trading volume. With this acquisition, CBOE will be able to leverage that European presence to accelerate the growth of non-U.S. trading of its products, particularly the options and futures based on its proprietary volatility indices. This past summer CBOE opened up an office in London, building on a global expansion plan that started with extending the trading hours of the CBOE Volatility Index options and S&P 500 index options to align with the market open in London.

New asset class

Still another dimension of this deal is in the foreign exchange arena. Bats is the owner of Hotspot, one of the leading electronic exchanges in the spot FX market, and plans to use this platform to expand into other types of FX products.

In November, Bats completed the acquisition of Javelin, a New York-based company that operates a swap execution facility. Although the SEF was originally built for the trading of interest rate swaps, Bats plans to use the regulatory license to trade non-deliverable forwards, a class of foreign exchange products that is being driven onto SEFs by the Commodity Futures Trading Commission.

On the cash equity side, Bats Europe is already the largest equities exchange operator in Europe, with a 23.6% market share in terms of volume, ahead of the London Stock Exchange with 18.1% and Euronext Group with 13.5%. In the U.S., Bats is ranked second in terms of market share, holding a 19.5% share of the U.S. equity markets in terms of volume.

"We get into two new asset classes that have always been one of our driving strategic initiatives," Andrew Lowenthal, vice president of options business strategy at CBOE, commented during a panel discussion at FIA Expo.

Bats technology

Another key aspect of the merger is the technology upgrade. CBOE earlier this year announced plans to upgrade its platform to a new system called Vector, replacing the current CBOE Direct platform that has been in use since 2001. Now, after the merger closes, CBOE plans to transition over to Bats technology.

Bats runs its markets on proprietary technology that is designed to maximize its appeal to the new generation of automated traders. Since its launch in 2007, Bats has reduced latency on its platform, the amount of time it takes to process an order message, to 57 microseconds from 930 microseconds, a reduction of 94%.

Bats also prides itself on working with its customers to offer innovative order types and risk management tools. For example, the exchange offers several products that enable its customers to monitor their order handling in real-time. These include its user dashboard and latency reports, which are web-based tools designed to provide real-time information about connectivity to the platform and the speed at which orders are processed and executed.

Since its launch in 2007, Bats has reduced latency on its platform to 57 microseconds.

The key man behind Bats technology is Chris Isaacson, a 38-year old software developer who grew up on a farm in Nebraska. Isaacson has been with Bats since the company's launch in 2005. He helped design the initial trading platform and now oversees all technology and market operations. After the merger is completed, Isaacson is slated to become chief information officer for the combined company. It will be his responsibility to guide the migration and assess what elements of CBOE's trading functionalities should be carried over.

Complementary market models

Despite the consolidation of ownership, the two exchanges will continue to operate multiple platforms in the equity options market that operate with different pricing models.

CBOE gets most of its business from a customer priority model, but it opened C2 to compete with maker-taker exchanges. Bats started from the opposite direction. Its initial exchange launched in 2010 was based on maker-taker, but its second exchange EDGX relies on the customer priority model.

In a sense, the merger is a convergence of two approaches to incentivizing liquidity. One model, which has its origins in the cash equity market, uses fee rebates to reward liquidity providers, while the other, more traditional model, charges market makers for the opportunity to access customer flow.

Rather than one model winning out over the other, market participants seem to prefer having the choice of multiple market models and pricing schemes. In a recent regulatory filing, Bats estimated that 28% of the total U.S. multi-listed options volume traded with price-time allocation, 43% of volume was in the customer priority/pro rata allocation model, and 29% was in complex orders.

On their own, each of the two exchanges was strong in one segment, but as a combined company, they will have significant share in two pricing models. Of course, that leaves complex orders — trades that require the execution of more than one contract at the same time — as the stronghold of other exchanges, notably ISE.

Look for the combined exchange to go after that segment once it completes its integration.