Oil futures trading took a dive in 2020 as the pandemic shut down the global economy and the demand for oil collapsed. Now that economies in many parts of the world are returning to growth, supply and demand for oil is moving back to normal patterns. The oil futures markets, however, have changed.

Confidence in West Texas Intermediate (WTI), the world's most actively traded oil futures contract, has been shaken by an extraordinary dive into negative pricing last year. The outlook for Brent futures, the most important global benchmark, is threatened by an inexorable decline in the underlying supply. Contracts on China's International Energy Exchange (INE) have plenty of volume, but these Shanghai oil futures are not yet accepted as an international benchmark. And a new exchange in Abu Dhabi has burst onto the scene with a focus on oil flowing from the Middle East to Asia.

Crude oil futures are the most heavily traded commodity futures in the world, so the outlook for the flagship contracts has a big impact on the industry. In this article, MarketVoice reviews the main strengths and weaknesses of several major contracts, starting with the newest entrant, the Murban oil futures traded on ICE Futures Abu Dhabi.

Fast start for Murban

The Murban crude oil futures began trading on 29 March. Volume picked up immediately, and in its first month around 50 firms had traded more than 163,600 contracts in total, equivalent to 163.6 million barrels.

It is still early days for this new contract, but its prospects look bright for several reasons. First, it has strong backing from the Abu Dhabi National Oil Corporation, the state-owned oil company of the United Arab Emirates. ADNOC is one of the largest producers of oil in the world, and it is keen to develop Murban, its flagship grade of crude oil, into a regional benchmark.

ADNOC moved to forward pricing of its crude oil in March 2020, using the Platts Dubai benchmark to peg its selling price. It has now switched its forward pricing mechanism for Murban to the ICE Murban futures contract from June, coinciding with the first expiry of Murban futures. It is also pricing three other grades of oil that it produces—Upper Zakum, Das and Umm Lulu—at a differential to the Murban price set by the futures contract.

Equally important, ADNOC has abolished destination restrictions for all its crude oil exports. In effect, this means cargos of Murban can be bought and sold many times over and redirected to whichever part of the world has the greatest demand. That is a key change from past practices among Middle Eastern producers, and it makes both the futures contract and the underlying physical commodity more attractive to the global oil trading community.

Second, the new contract is directly tied into physical flows. The ICE Murban futures are physically delivered contracts, with one futures contract equaling 1,000 barrels of Murban crude delivered from ADNOC's storage terminal in the port of Fujairah, which provides direct access to the Gulf of Oman. ADNOC is spending around $900 million to build 42 million barrels of storage space in caverns beneath Fujairah’s mountains. That storage space, and tanks that it already has at the port, will ensure there is plenty of Murban on hand to manage any future supply disruptions, Khaled Salmeen, the company’s head of marketing and trading, told Bloomberg reporters in March.

Third, the new exchange, ICE Futures Abu Dhabi, has strong backing from key players in the global oil markets. Nine of the world's largest oil companies and traders have joined IFAD as founding partners, including Thailand’s PTT, Japan’s Eneos and Inpex, South Korea’s GS Caltex, PetroChina, BP, Shell, Total and Vitol. The participation of the Asian companies is particularly important, in that it reflects the role of Asian refineries in buying crude oil from the Middle East and their interest in developing a futures contract based on those trading flows.

Fourth, IFAD leverages the existing market infrastructure built by the parent company, Intercontinental Exchange. That includes a well-established ecosystem of brokers, market makers and clearing firms connected to its trading and clearing platforms as well as a large complex of actively traded futures and options based on crude oil and refined products. For example, the new Murban contract is cleared through ICE Clear Europe, the same clearinghouse used for Brent futures. That makes it an easy lift for clearing firms to support the new contract and it helps explain why 18 clearing firms were signed up before the launch.

"We, along with our clients, are excited for the extraordinary opportunity that the launch of Murban futures presents," John Murphy, global head of futures at Mizuho Americas, said in March. "This moment signifies a tremendous progression for the oil markets, and we are ready and eager to clear IFAD products."

The Middle East is a key crude supplier to Asia, exporting more than two thirds of its oil to the region. Abu Dhabi hopes that its futures contract will become a key pricing reference for Asian refiners who are likely to drive crude demand in the coming years. A big challenge, however, will be to convince market participants that a new crude benchmark is actually needed.

There are several other regional benchmarks already in use. S&P Global Platts, for instance, publishes price assessments for oil produced in Dubai and Oman, and the Dubai Mercantile Exchange trades futures for Omani crude. Both act as benchmarks for Middle Eastern shipments to Asia.

In addition, it is unclear if other Persian Gulf producers will want to make further changes to their crude pricing practices in the near future, according to analysts at Argus Media. Saudi Arabia switched from assessments published by Platts to futures contract prices published by DME for the Oman component of its export pricing formula in 2018. This move was followed by Bahrain and Kuwait.

IFAD also faces competition from another crude oil futures market emerging in Asia—the Shanghai International Energy Exchange.

Shanghai gains traction

China launched the INE in 2018 with the goal of developing its own benchmark for oil prices. China is the world's largest buyer of oil, and the crude oil contract was developed to give China more of a say in the pricing of imported oil.

The INE crude oil futures contract is based on 1,000 barrels of oil, the same size as the WTI and Brent futures, but unlike those contracts it is denominated in Chinese yuan rather than the US dollar. To encourage international adoption, the INE allows direct participation by foreign traders and brokers, a first for a mainland Chinese futures exchange.

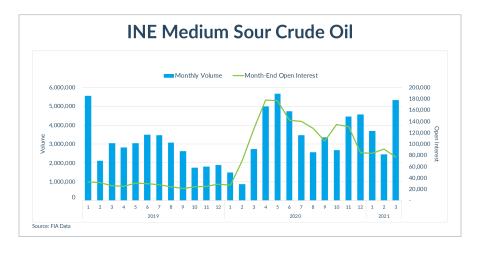

The INE contract has been successful in terms of trading volume. In the first three months of 2021, over 11 million contracts traded, more than double the amount in the first quarter of the previous year. In comparison, the two most heavily traded oil futures in the world—the WTI futures traded on the New York Mercantile Exchange and the Brent futures traded on ICE Futures Europe—both had approximately 67 million contracts traded in the first quarter. In effect, the Shanghai contract has roughly one-sixth of the trading volume of its global peers, an impressive feat for a contract and an exchange that are less than three years old.

One challenge, however, is that most of that trading seems to be speculative. Open interest, the industry term for the number of contracts outstanding, is generally viewed as an indicator of commercial participation in a market. For example, open interest includes positions held by producers using futures to hedge their market risk and by dealers using futures to manage the risk in their trades with counterparties. At the end of March, open interest in the Shanghai contract was less than 100,000 contracts, whereas the open interest for the WTI and Brent contracts was more than 2 million each.

Furthermore, the volatility in the oil markets last year exposed constraints in the infrastructure needed for physical delivery of oil tied to the futures contracts. During April 2020, prices for INE futures were trading at a premium to both WTI and Brent, but physical traders were unable to respond to the demand because the exchange's storage facilities were at full capacity.

The INE moved quickly to address this issue. By April, the exchange had increased its total storage capacity to nearly 48 million barrels, adding new tanks in Shandong, Hainan, Guangdong and Liaoning and allowing for a total of 14 delivery points. According to analysis published by the Oxford Institute for Energy Studies, the expanded infrastructure will allow for increased volumes of physical deliveries and expand the futures contract's appeal to "independent refiners, the most dynamic part of the Chinese market."

The Institute also commented that the expanded infrastructure should encourage more established foreign traders to deliver into the INE contract. Evidence of this trend emerged in July, when Reuters reported that two large international oil trading companies—BP and Mercuria—delivered cargos of oil into the INE contract. In a further sign of international involvement, an oil facility in the port of Qingdao that is part owned by Mercuria was approved by the INE in February 2021 as an additional storage location.

Brent grapples with production decline

The Brent futures contract traded on ICE Futures Europe is the most widely used gauge for oil pricing. ICE estimates that roughly 63% of all oil traded on the spot market globally is priced based on Brent. And the futures contract is supported by a large complex of related products that provide market participants with efficient ways to trade the spreads between different delivery locations, various grades of oil, and an array of products refined from crude oil.

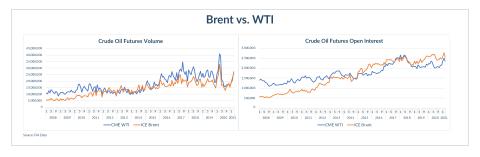

The Brent futures contract also is gaining ground on its main competitor, the WTI futures traded on Nymex. Historically the WTI contract was the most heavily traded futures contract in the energy markets, but over the last several years the two contracts have been neck and neck in terms of trading volume and Brent has moved slightly ahead in terms of open interest.

The Brent market faces a significant challenge, however. The benchmark on which the futures contract is based is measured by physical trading in a basket of five grades of oil produced in the North Sea. The production of those grades of oil is steadily declining. That leads to fewer transactions in the physical market, and greater risk that the benchmark may not be as reliable as it used to be.

The Brent 'ecosystem' can be divided into four layers: the spot market for what is known as dated Brent, the forward market, the futures market, and the swaps and options markets. Dated Brent is used globally and set daily by S&P Global Platts.

When the Brent benchmark was first adopted for widespread use in 1985, the oil came from Shell’s Brent oil field. But as production diminished, crude oil from other fields in the North Sea was added into the blend that makes up the benchmark: Brent, Forties, Oseberg, Ekofisk and Troll (BFOET).

But the output from those fields continues to decline, and Platts has been exploring whether new sources of crude can be added to the Brent basket. One option is the Johan Sverdrup field off Norway, which is productive enough to shore up concerns regarding Brent's liquidity. That oil, however, is heavier and sourer than other BFOET grades, which would undermine Brent's position as a benchmark for light sweet crude. Further afield, Russia's Urals crude is relatively accessible and abundant, but it also comes with issues relating to its sulfur content. Meanwhile, West African grades are more remote and less transparent, with frequent disruptions to supply and different loading cycles.

In an effort to solve this issue, Platts announced in February that it would add WTI Midland, a light sweet crude oil produced in West Texas, to the grades underlying its benchmark from July 2022. Vera Blei, the head of oil markets pricing at Platts, explained that exports of WTI Midland had become a "mainstay" for European refiners and the addition would ensure the "continued robustness of the Brent complex for the next decade and beyond."

A month later Platts did an abrupt reversal and shelved the plans "for an undefined period" following industry backlash. The main cause of contention was not the addition of US production, but rather a proposed change in the pricing methodology. The plan was to include the cost of freight and related expenses, known as CIF [cost, insurance, and freight], that are required to deliver the oil to Rotterdam, the main point of entry for the European market. That contrasts with the current approach, which is calculated on an FOB [free on board] basis, i.e., the price when the oil is loaded at a terminal in the North Sea. Many market participants objected to this switch because of its impact on pricing relationships within the Brent complex and the added risk of changes in freight costs.

Platts has not given up on changes to the Brent basket. The price reporting agency said it plans to form an industry working group to consult on how to include WTI in the Brent complex as well as any other alternatives. Until this is resolved, however, the decline in the production of Brent crude creates some uncertainty for this benchmark, especially for market participants looking to manage market risk far into the future.

On the other hand, the deep liquidity of the Brent complex makes it tremendously appealing to traders. And some market observers downplay the concerns about production, saying that it can continue to serve as a pricing reference even if the underlying supply continues to dwindle.

"Brent is still the most relevant as a global market, particularly as it prices West African crude which is the key swing between Europe and Asia. It also benefits from already having liquidity and depth of volumes along the curve which makes it very hard to displace," said Paul Horsnell, head of commodities research for Standard Chartered.

"The output of the underlying grades is not a straightforward issue—in short it becomes a problem when the market worries that it is affecting the reliability of price formation," Horsnell added. "Dubai managed to survive as a useful market for 25 years on very low volumes, and ANS delivery Gulf Coast was used as a marker for exports to the US for a few years after the flow of physical cargoes into the Gulf had fallen to zero. In other words, something with twice the volumes is not necessarily twice as good as a marker."

US exports boost WTI

On April 20, 2020, the price of WTI futures hit a historic low around negative $37 per barrel. This was partly driven by the macro-economic factors that depressed oil prices worldwide, namely, the demand destruction caused by the pandemic and over-production by Saudi Arabia and Russia. But it was also due to the specific characteristics of the contract.

"The negative WTI price occurred on a single day last year ... such a short-lived event cannot have an impact on the hedging program of any oil producer. We see no evidence that hedging was performed with the use of other oil benchmarks." - Georgi Slavov, global head of fundamental research at Marex Spectron

Expiring futures are settled through the delivery of oil into a huge network of pipelines and oil tanks centered in the town of Cushing, Oklahoma. As the front-month futures contract approached expiration, buyers discovered that there was not enough space to cover all the oil that was due to be delivered. In their scramble to sell down their positions before expiration, they drove the price well below zero.

The negative pricing lasted only briefly, but it shook confidence in the reliability of the WTI futures as a benchmark for oil prices. Market participants are now keenly aware of the contract's link to local market conditions in the US and the potential storage challenges around settlement. That contrasts to Brent, which has more flexibility in how it can be stored.

"While Brent's nominal storage capacity is lower than WTI at Cushing, it is intrinsically linked to the global market, with the crude making up the Dated Brent benchmark easily deliverable by tanker to refiners in any continent," wrote S&P Platts analyst Richard Swann shortly after the negative pricing incident.

On the other hand, the WTI futures market remains extremely liquid, with a large and diverse population of market participants as well as a host of related futures based on price relationships across the energy complex. That makes it the "most efficient" way to trade oil, according to CME Group, the parent of the Nymex exchange.

The WTI futures market also benefits from the explosion in US oil production over the last decade driven by new techniques for extracting oil from shale formations. That makes it the centerpiece for hedging by US producers and others that rely on this source of oil.

“The negative WTI price occurred on a single day last year due to the negative demand shock in Q1 2020 and the subsequent spike in inventory. However, such a short-lived event – less than one trading day – cannot have an impact on the hedging program of any oil producer,” said Georgi Slavov, global head of fundamental research at Marex Spectron. “In addition, the consistent decline in oil prices which started in early January 2020 triggered a sharp increase in hedge ratios. Historically, US oil production is about 30-35% hedged. This rose to 45% this time last year before retreating to the long-term average levels. Lower output and a steady uptrend in prices also contributed to the decline in the hedging ratio. We see no evidence that hedging was performed with the use of other oil benchmarks,” he said.

Going forward, US oil exports are becoming increasingly important to the global market. Platts proposed adding WTI Midland to the Brent basket because of its importance to European refineries. US oil also is flowing to buyers in Asia. In 2020, US exports of crude oil to China jumped to 176 million barrels of oil, more than three times the amount in 2019 and more than any other destination, according to the Energy Information Administration, a branch of the US Energy Department.

Case in point: During the peak of the oil market over-supply in early 2020, Hess, one of the largest independent oil producers in the US, chartered three very large crude carriers to store six million barrels of oil coming out of its fields in North Dakota. The company disclosed during a briefing for investors in January that one of the cargos was sold to China in September; the other two were sold to China several months later.

The key question is whether these US exports are priced with reference to WTI or Brent. Hess currently relies on WTI futures to hedge most of its production, but these three cargoes were all sold at a premium to Brent. It will be interesting to see how US producers adjust their hedging strategies as the market continues to evolve.

Both ICE and CME have attempted to address this issue by introducing futures contracts based on the price of oil being exported from the Gulf Coast—the Permian WTI (HOU) contract and the WTI Houston (HCL) contract respectively. Trading volumes have been relatively low, however, and these contracts show no sign of dislodging WTI futures as the primary gauge of US crude prices.

Will Acworth contributed to this report.