The liquefied natural gas (LNG) industry’s emergence as a distinct hydrocarbon market has accelerated in 2019.

Having historically been seen as a product that traded solely on long-term contracts indexed against oil and natural gas prices, LNG is maturing from its position as “junior partner” to become a mature commodity with its own dynamic spot market. The LNG spot market accounted for 25% of total trade in the product in 2018, versus 20% the year prior, according to the International Group of Liquefied Natural Gas Importers.

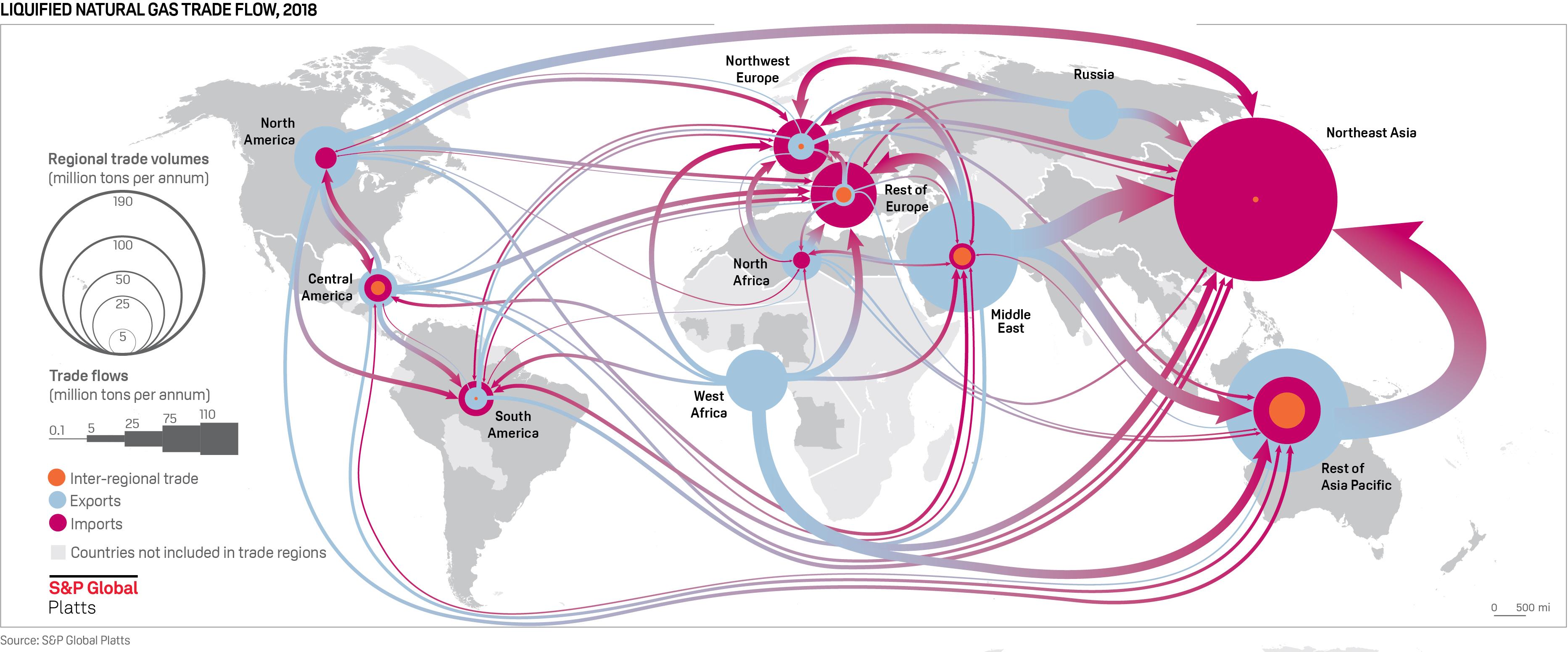

LNG’s pricing increasingly reflects what LNG is: the option to import gas into countries where there is demand for natural gas but insufficient ability to access gas through pipelines. This option is being treated with ever greater precision thanks to three closely related trends: 1) the emergence of a liquid spot market into Northeast Asia (more than half of total spot activity in 2018 was into Japan, South Korea and China), 2) increasingly efficient decision-making and flexible contract structures, and 3) higher market transparency thanks to the emergence of price formation processes.

Simultaneously there is the emergence of a bustling market for LNG derivatives as a tool for managing price risk. In fact, the value of notional open interest in LNG derivatives has moved above that of thermal coal, its main competitor in the seaborne market for power generation fuel.

LNG’s blossoming as a separate market is particularly visible in the recent dislocation of LNG spot prices from crude oil and natural gas benchmarks as well as the increase in LNG derivatives trade volumes.

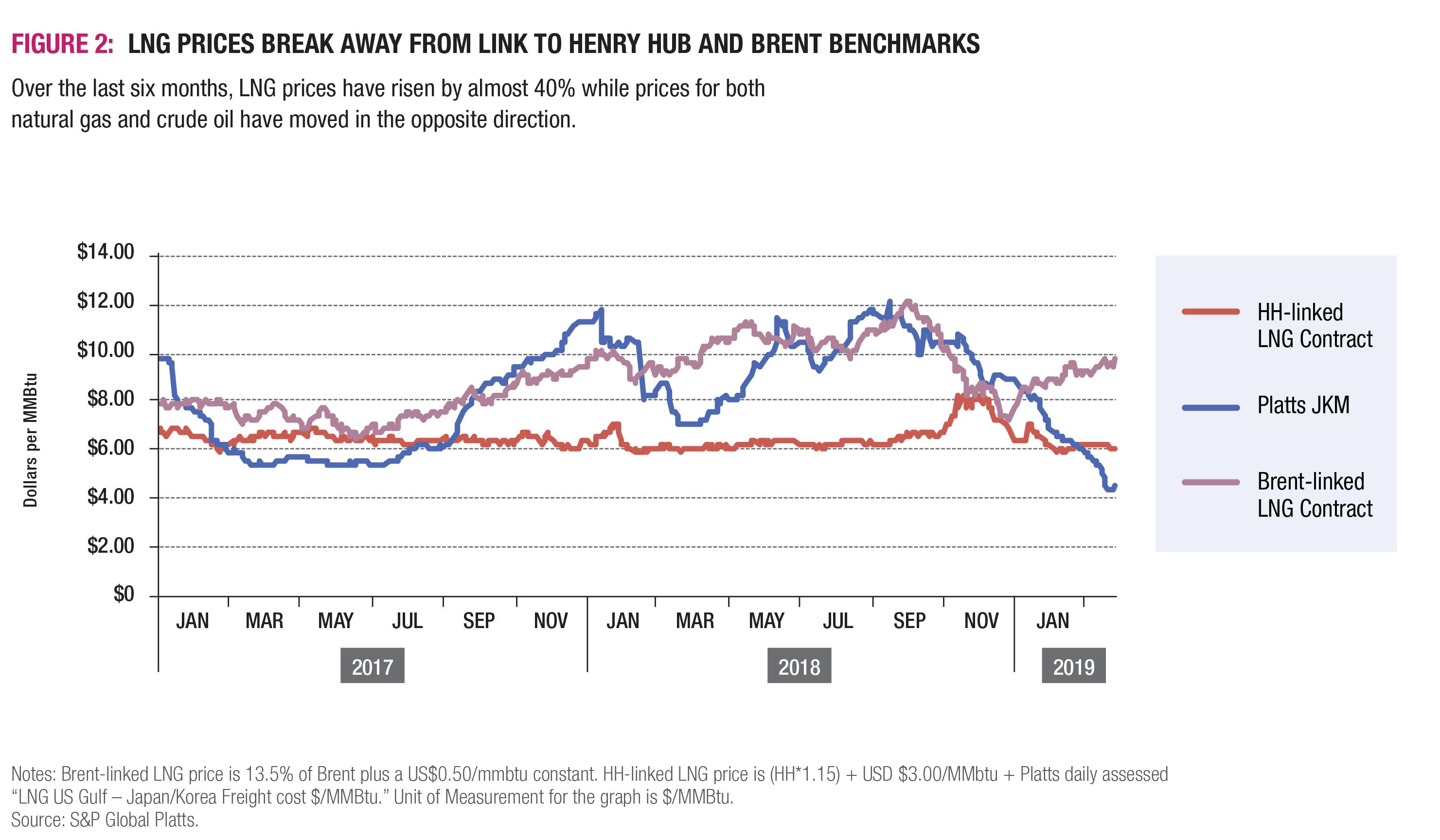

The LNG price used for comparison here is the Platts Japan Korea Marker, or JKM. This benchmark is the world’s longest-running daily price assessment for physical LNG spot cargoes delivered into Northeast Asia – the largest demand area globally for LNG.

LNG’s price has sharply moved away from long-term contract formula prices based on Henry Hub natural gas and Brent crude oil this year [Figure 1]. This is significant because long-term LNG contracts historically were priced off Brent, and more recently commissioned contracts for US-origin supply have been priced off Henry Hub.

In fact, LNG prices are now inversely correlated to Brent crude oil prices. In Q1 2019 LNG ran a negative 90% correlation to Brent, versus a positive 88% correlation in 2017. Meanwhile, LNG prices are at their steepest discount on record to equivalent Henry Hub-related long-term contract prices: touching minus $2.81/MMBtu in late March.

Swings away from Brent and Henry Hub prices mean that long-term off-takers suffer losses if selling the same cargo onto the spot market, while utility companies buying via long-term contracts have an equivalent opportunity cost. In March 2019, for example, a company agreeing to buy a cargo on a DES Northeast Asia basis from the US could expect to have a long-term contract price of around $7.30/MMBtu; for that same company the price available for sale in the near-term market would have been around $5.20/MMBtu on average.

Combining the dislocation of LNG prices from crude oil with Brent’s usage in long-term contracts can also create unique incentives for near-term off-takers. In normal market conditions, a larger cargo of any commodity would command a discount to a smaller cargo due to economies of scale; but due to the current crude oil-LNG pricing mismatch, traders are incentivized to pay up for a larger fixed price cargo in order to maximize their opportunity to sell into a Brent-related short with as much volume as possible.

This pricing dislocation is bringing about difficult conversations between buyers and sellers at a time when the LNG price is at a three-year low on the back of a wave of new supply, which is not being met by an equally strong demand growth in the main LNG-consuming Asian markets.

New liquefaction projects in Australia, Russia, and the US are expected to add over 20 million tonnes per annum of LNG in 2019, growing the LNG market by 8% in one year versus a forecasted average annual growth rate of 3% over the next 20 years.

Continued growth of LNG demand, even with the help of China, is not able to accommodate such a rapid build-up of supply. Spot prices for LNG thus declined, and will need to stay low enough to incentivize incremental demand, e.g. by replacing coal-fired power generation in Europe. A period of limited new LNG supply in 2021-23 has the potential to reverse this cycle, with significant new supplies from 2024 onwards only to see the market likely returning to lower prices and significant LNG flows to liquid European gas markets.

Platts Analytics expects the pricing of LNG to increasingly reflect its own fundamentals, while taking strong guidance from the key global pipeline gas benchmarks of Henry Hub in the U.S. and the TTF and NBP gas hubs in Northwest Europe. Strong distortions and significant volatility of how spot LNG is priced versus the oil-indexed long-term contracts will create significant market opportunities, but also distress for buyers. A similar development as in Europe, where contract renegotiations and arbitrations made way to gas-to-gas competition, seems likely and warranted.

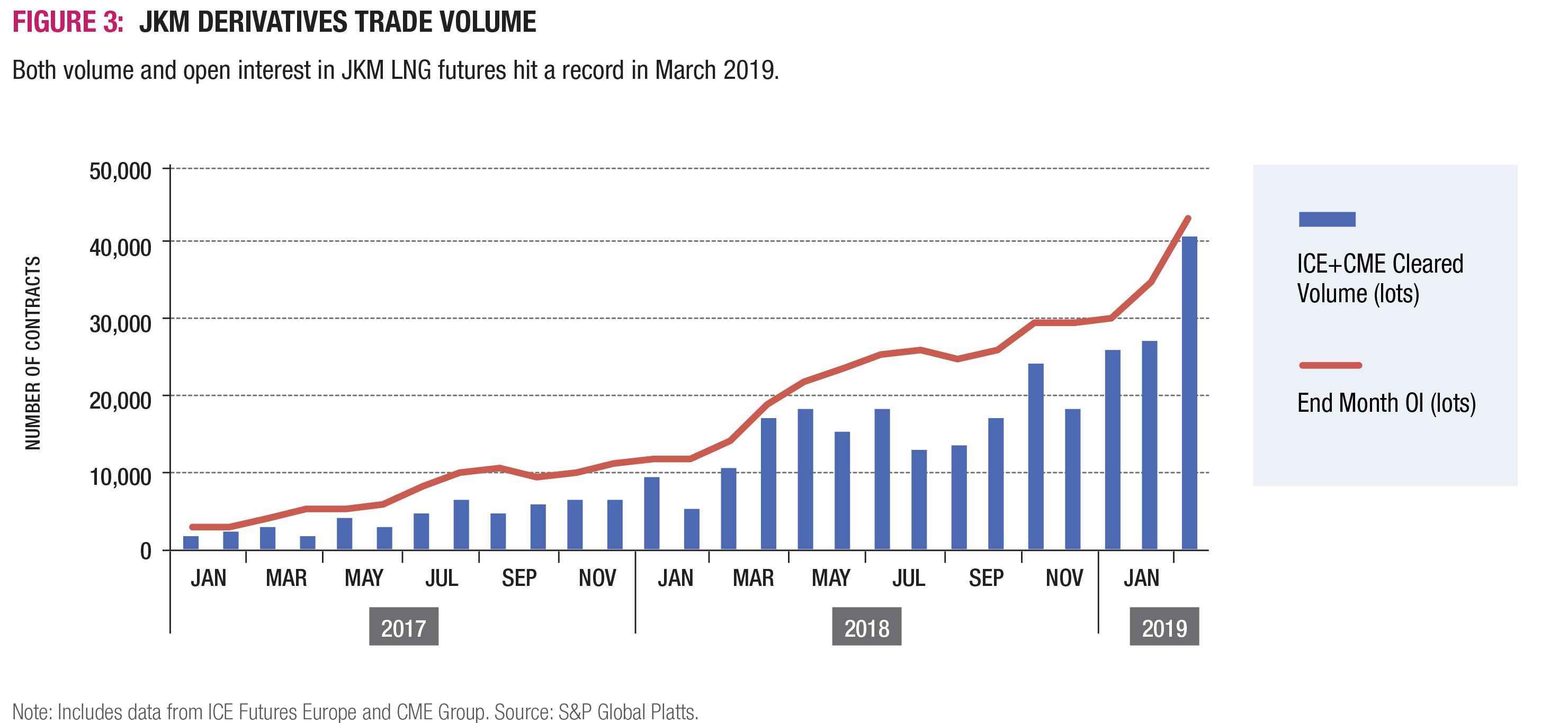

This move towards pricing independence has created demand for LNG derivatives as a tool for managing price movements. Currently the most liquid LNG derivatives is the JKM futures contract, which settles against the monthly average of Platts JKM and clears through Intercontinental Exchange and CME Group. In the first quarter of 2019, trading in this contract surged 367% year-on-year.

Another way to look at this is comparing the derivatives trade volume against the total size of the physical LNG market. In March 2019 the cleared derivatives trade volume equated to 27.7% of the total physical market; in March 2018 paper trade amounted to only 7.7% of the physical market size.

A surge in paper trade is hardly surprising when one considers the annualized volatility of JKM during Q1 2019, or the fact that LNG’s relationship to other hydrocarbons split in the same time period (a significant portion of derivatives trade has been inter-product spreads, i.e. LNG-to-gas hub). However, the open interest on these derivatives contracts has continued to grow significantly in 2019. This indicates that the exposure to spot market pricing in the physical LNG market has swelled. Another hint from the forward curve of deeper JKM-related exposure is the fact that trade for longer tenors has increased at a quicker rate than total derivatives trade. Trades for whole calendar year periods out to 2021 have increased as a proportion of total derivatives trade to nearly 10% in 2019, for example.

As the forward curve builds out and paper volumes ramp up, the complexity of derivatives products on offer has also deepened, with the first cleared JKM options trades taking place in March.

How Platts assesses LNG prices

S&P Global Platts uses the Market-on-Close (MOC) methodology to assess JKM, which represents the daily tradeable price of spot LNG cargoes delivered into Northeast Asia.

The MOC is a structured day-long process that ends at 4:30pm Singapore time – the timestamp for Platts LNG assessments in Asia, and is an assessment process adopted widely across energy markets.

During the MOC assessment process, Platts publishes real-time information from active market participants that report firm, named bids, offers and trades in order to test market value and form a representative price assessment at the close of each trading day.