During the fourth quarter of 2021, FIA and Coalition Greenwich, a consulting firm specializing in financial services industry, jointly conducted a survey on a wide range of topics related to the trading and clearing of derivatives. The survey received more than 180 responses from market makers, brokers, clearing firms, exchanges, clearinghouses and other types of firms.

Buyside insights

One of the most important features of the survey was feedback from asset managers and other "buyside" users of derivatives. These firms mainly use derivatives to hedge their market risks, and the survey showed they have stepped up their use of clearing, particularly for over-the-counter derivatives such as interest rate swaps.

One of the top issues facing buyside firms is the transition away from the use of Libor in the interest rate markets. Although this transition has been ongoing for some time, market participants are coming under increasing pressure to switch to alternative reference rates, and in some markets such as the UK, the use of Libor has been completely phased out. This is causing major changes not only on trading desks but all the way through operational systems on the buyside.

Also top of mind for the buyside is the requirement to post margin on uncleared derivatives. This requirement is being implemented in phases, and the deadline for compliance is coming later this year for most asset managers, hedge funds and other end-users. Putting these requirements into effect will require many changes to counterparty relationships, collateral management and other parts of the trading and clearing process.

In a related finding, most buyside respondents said they expect to see a decline in the use of uncleared derivatives that are subject to this new requirement and an increase in the use of clearing. When asked where they would like to see more availability of clearing, the buyside respondents pointed to interest rate swaptions, cross-currency swaps, total return swaps and single name credit default swaps.

An increased use of clearing will lead not only to more transaction flow through clearinghouses but also more reliance on clearing firms to process trades, collect collateral to meet margin requirements, and guarantee client positions at the clearinghouses. When asked what factors are most important to measuring the quality of their relationships with clearing firms, buyside respondents put "quality of execution" first, followed by fees, access to markets and products, and quality of operational processes.

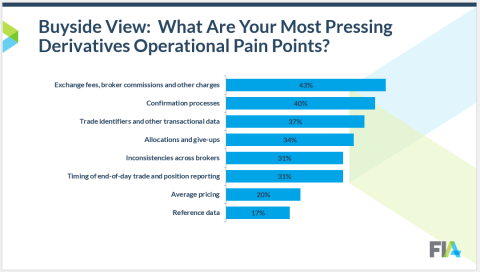

Operational processes have come into focus for FIA members over the last several years as surges in volume have exposed bottlenecks in the post-trade process. To shed more light on this issue, the survey asked for feedback from the buyside on the most pressing pain points in derivatives operations. The survey revealed a cluster of problems with roughly equal weighting: exchange fees, broker commissions and other charges; confirmation processes; trade identifiers and other transactional data; and allocations and give-ups.

Sellside insights

Turning to the sellside, the responses from clearing firms, executing brokers and other intermediaries showed some areas of agreement with the buyside but also some areas of different emphasis. For example, when asked for their views on the top three issues facing the industry, the sellside respondents put the highest weight on the impact of capital requirements. This reflects one of the long-term consequences of the 2008/2009 financial crisis; higher capital requirements on the banking industry have reduced the potential for systemic risk, but they also have increased the cost of providing clearing services to clients.

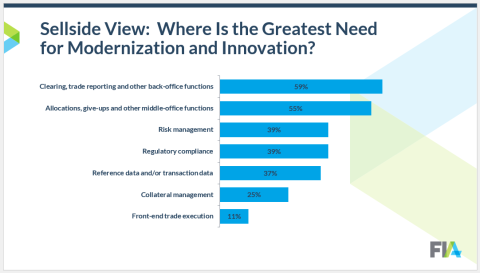

The survey also showed that the sellside shares the concerns of the buyside about the quality of operational processes. For years, the sell side has invested in better and faster tools for executing trades, but the pendulum has shifted. The survey respondents said that it is now the less glamorous functions such as clearing, trade reporting, give-ups and allocations that have the greatest need for modernization and innovation.

There are some important regional differences, however, in where clearing firms are investing for change. Most clearing firms are targeting improvements to their internal workflows, but after that there was a distinct difference by region. In North America, clearing firms put a relatively high priority on improving their ability to monitor costs and profitability. In contrast, clearing firms in Europe and Asia-Pacific put a higher priority on adding new products and connecting to new clearinghouses. This reflects several important changes in the landscape of clearing in those regions. In Asia-Pacific, the steady opening of the onshore China futures markets has created new opportunities for global clearing firms. And in Europe, the fallout from Brexit has triggered shifts of both clients and liquidity into continental European markets.

Looking at three specific areas of potential growth for the industry, the survey revealed that clearing firms and other intermediaries are building up their capacity to support cryptocurrency futures, carbon futures, and the onshore China markets. Roughly 40% of the sellside said that their firms are already committed to these markets, and another 10% to 20% said their firms plan to enter in the near future.

Asset managers, on the other hand, appear to be holding back. In all three areas, only a minority of buyside respondents said that their firms were already active. Most said their firms are "watching with interest" but not yet committed, or they dismissed it altogether. This was particularly true of cryptocurrency futures. More than half of the buyside respondents said digital asset markets are "not relevant" to their firms.

Access the full report here.