A dynamic interest rate environment has revitalized an important segment of global derivatives markets. Total trading volume in interest rate futures and options is running far ahead of last year's pace, and if trends hold up, this segment of the global ETD markets should smash last year's record.

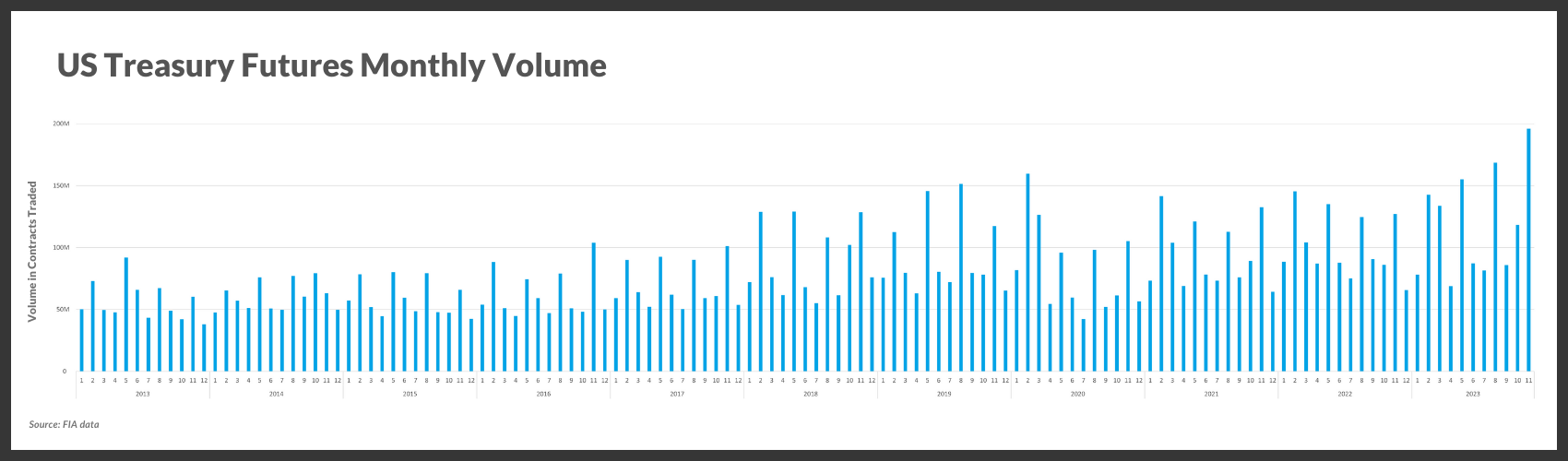

This growth trend is most evident in CME-listed contracts linked to US Treasury markets. When the Covid-19 pandemic hit in 2020, the sudden reversal in economic outlooks and market sentiment led to massive spikes in trading volume in virtually all interest rate contracts. For several years afterwards, the Treasury futures markets remained relatively quiet, but this year trading has taken off.

Total volume across all CME Treasury futures hit a record of 168 million contracts in August, and then set another record of 196 million contracts in November. That compares to 160 million in March 2020, and just 60 million contracts 10 years ago in November 2013.

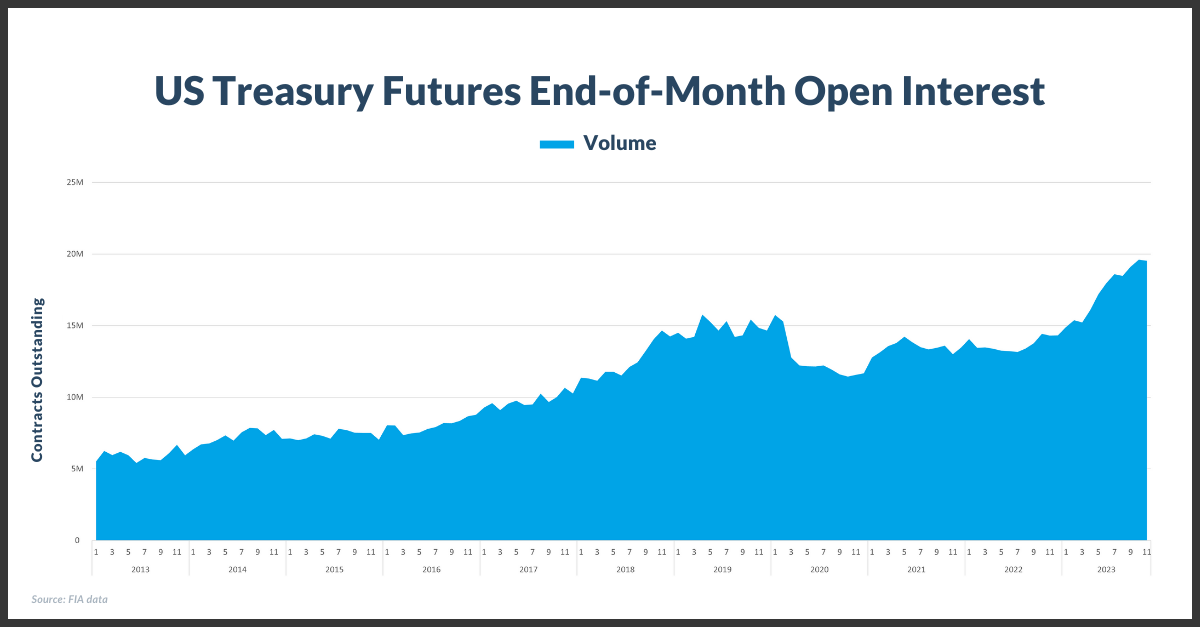

Trading volume isn't the only metric on the rise, however. Open interest, which measures the number of outstanding contracts, has been rising steadily since the fall of 2022 and has been breaking records since May. As of the end of November, open interest for all Treasury futures listed on CME had surpassed 21 million contracts, an all-time high.

"Throughout 2023, we have seen record volume and open interest in our U.S. Treasury futures, which offer market participants the most efficient and liquid products to hedge risk across the yield curve," said Agha Mirza, CME Group's global head of rates and OTC products.

All three of the main Treasury futures contracts - specifically, the contracts tied to 2-year, 5-year and 10-year notes - have seen strong growth in open interest this year. However, the 2-year contract is in a class by itself. Open interest as of the end of the third quarter was double last year's level.

The surge in trading activity and position taking was not surprising, given uncertainty about the long-term outlook for interest rates. Back in March 2022, US Federal Reserve officials enacted the first of what would become a series of eight interest rate increases. That prompted regional banks, mortgage lenders, asset managers, hedge funds and many others to load up on Treasury futures, either to limit their exposure to the risk of rising interest rates or to add more exposure to their investment portfolios.

The Fed appears to have put the rate hikes on pause, and now the markets have begun to wonder when it will become less hawkish and start taking rates back down. In such an environment of uncertainty, derivatives are in high demand.

In a recent presentation to investors in CME stock, Terry Duffy, the company's chief executive, highlighted the importance of futures for risk management. “With so much uncertainty in the world we live in, we're continuing to work closely with our clients to help them navigate uncertainty and manage their risks...Regardless of whether rates rise, fall or hold steady, the shape of the yield curve and interest rate views continue to shift, and our customers need to manage that risk,” said Duffy.

CME has no control over the future path of interest rates, of course, and no way to know what demand for risk management will look like next year. But the exchange is taking steps to make its Treasury complex more attractive.

Recently the Treasury Department stepped up its issuance of Treasury bills, which mature in one year or less. In response, CME added bill futures to the array of Treasury futures that it offers. The contract immediately attracted interest from traders, with roughly 40% of the trading executed as a spread against SOFR futures, the benchmark for interest rates in the money markets.

CME also is looking to reduce the cost of trading by implementing several enhancements to its cross-margining agreement with the Depository Trust & Clearing Corporation, the main clearinghouse for the cash Treasury market. The cross-margining program can be used by firms that are members of both clearinghouses to calculate margin based on the combination of their positions in Treasury securities and CME interest rate futures. When positions on one side offset the risks on the other side, the amount of required margin is reduced.

During CME's recent investor presentation, Tim McCourt, global head of financial and OTC products at CME, commented on how the cross-margining program could impact the trading of Treasury futures. “When you unlock the capital efficiencies of related products, it significantly increases the risk management capabilities of the marketplace and can lead to increased trading velocity in the product,” said McCourt.

CME and DTCC say that there are about 30 firms that are eligible for this cross-margining program. The enhancements, which will go live in January, expand the range of CME futures eligible for the program and give the firms more flexibility in deciding which contracts they want to include in the margin calculations.

McCourt compared the impact of the upcoming enhancements to a separate margin offset program for interest rate swaps cleared by CME that was put in place in 2012. He commented that the average daily savings have grown from $1 billion in 2013 to $7.5 billion in 2023. "At that same time, our rates volume grew 109%, and open interest doubled in the complex...Unlocking capital is beneficial to the volume and the velocity of the complex, and we're optimistic about what we can do once this comes online early next year.”