Over the last five years, a growing number of equity swaps have migrated to the central counterparty operated by Eurex, the largest derivatives exchange in Europe. Rather than using existing equity index futures, market participants instead are using "total return futures" that are designed to replicate the return profile of an equity swap traded bilaterally in the over-the-counter markets.

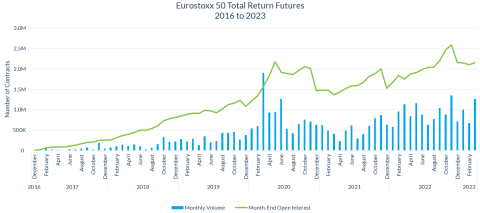

When Eurex introduced total return futures on the Eurostoxx 50 in 2016, there was not much trading at first, but gradually it increased, with a big jump during the pandemic and another surge in 2022. In the first quarter of this year, trading volume has averaged around 45,000 contracts per day, up from 43,000 over the course of 2022 and more than four times the level in 2020.

More importantly, open interest has been rising steadily, a sign that banks, asset managers and other market participants are holding larger positions at the Eurex clearinghouse. After peaking at around 2 million contracts in the second quarter of 2020, open interest in the Eurostoxx TRF dropped below 1.5 million in 2021, and then steadily rebounded. OI reached a record level of 2.6 million in November 2022, and it has remained above 2 million contracts every month since then.

In fact, in March of this year, open interest in the total return future actually surpassed the open interest in the conventional Eurostoxx 50 future. Not because the conventional contracts are losing ground, but rather because the total return future has created its own place in the risk management toolkit.

What is driving this steady growth? The main driver is UMR, the acronym that refers to the regulatory requirements to collect initial margin on uncleared derivatives. These requirements were drafted by policymakers after the financial crisis of 2008 with the idea of reducing the risks in the over-the-counter derivatives markets. Requiring initial margin on these contracts creates a buffer against losses from market moves. It also creates an economic incentive to switch to central clearing. That is because the margin requirements on derivatives held at clearinghouses are generally lower than derivatives that are traded on a bilateral basis, i.e. between two dealers or between a dealer and an asset manager.

From the perspective of participant in the OTC equity swap market, switching to total return futures provides significant capital efficiencies. Total return futures can be netted against each other, with short positions offsetting long positions, which means the margin requirements apply to the net rather than gross exposure. The margin requirements are further reduced by offsets with related contracts, such as the conventional Eurostoxx 50 future and other equity derivatives cleared by Eurex. And like all contracts cleared by a central counterparty, the users benefit from the reduction in counterparty credit risk.

The UMR requirements did not take effect immediately after the crisis. Instead they were phased in over time, starting with dealer-to-dealer trades in 2016 and then gradually extending to clients. Phase 5, which covered asset managers and other clients with more than €50 billion in OTC derivatives, took effect in September 2021. Phase 6, which applies to clients at the next level down in terms of size, took effect in September 2022. As a result, UMR now applies to the majority of OTC derivatives trading worldwide.

As early as 2015 dealers began looking for ways to reduce the margin requirements on their OTC positions, and they approached Eurex with the idea of creating a new set of futures contracts that would replicate the equity swaps they traded bilaterally. Conventional equity index futures track the price of an index. Equity swaps, however, track the entire return from the underlying stocks, including dividends and financing costs.>

Eurex therefore created total return futures that combine the price return on the Eurostoxx 50 index with the value of the dividend distributions and the financing cost. That cost is defined as a spread over the benchmark for short term interest rates, which currently is the €STR benchmark.

Unlike the conventional Eurostoxx 50 contracts, the total return futures generally do not trade through the on-exchange order book. Instead they are negotiated off-exchange, usually as a spread over the conventional futures, and then booked into the exchange through its trade entry system.

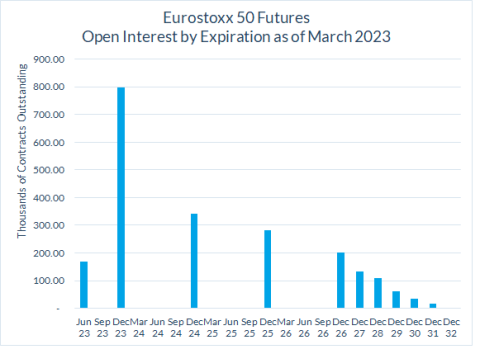

The institutional character of this market shows up in the distribution of open interest. Data from Eurex shows that more than half of the open interest at the end of the first quarter was held in contracts that mature in 2024 and beyond, with some open interest going all the way out to 2032. That reflects the use of these products to hedge the risk in structured products that provide long-term exposures to stock market returns.

The connection to the structured products market is a key driver for the growth in the total return futures. Structured products typically are designed to provide retail investors with a return linked to the performance of equity markets but also the protection of principal similar to owning a government bond. That protection typically comes through embedded options that set a floor on the potential loss but also reduce some of the upside. According to a January 2023 report by the European Securities and Markets Authority, retail investors in Europe had €330 billion invested in structured products in 2021.

The issuers of these products, typically banks, can use TRFs to hedge the long-dated forward exposure that they take on when selling these products to investors. The most common term for these products is 10 years, which means that banks need to hedge the risk that a market move at any point in the next 10 years might trigger the embedded options. In addition, they need to hedge changes in the dividend distributions, given that those are also embedded in the returns that investors receive.

In effect, the total return futures leverage the price discovery function of the conventional Eurostoxx 50 future, which is the most actively traded equity index future in Europe, while providing its users with the same return profile as a bilateral total return swap.

Another key driver is the value of these futures in hedging uncertainty about dividend payments. This was especially important in 2020, when the pandemic triggered a drastic reduction in economic activity worldwide and many companies abruptly reduced or eliminated their dividends. And it has continued to be a factor as economies reopened and dividends started rising again.

The Eurostoxx 50 index is designed to include the largest corporations in the Eurozone, and these companies tend to pay relatively large dividends. An asset manager that buys a total return future has the certainty of knowing that the return on that position – for however long it is held — will include all dividends paid by the companies in that index. In contrast, buying the conventional future creates some basis risk – i.e., a divergence between the value of the index and the returns from owning the underlying stocks. That was one reason for a big spike in both volume and open interest in the Eurostoxx TRF in 2020.

Still another driver is the opportunity to trade both types of contracts as a way to isolate the financing cost embedded in the total return future, also known as the repo rate. A trade that combines a short position in the conventional contract and a long position in the TRF will be neutral to changes in the value index, but it will give the holder of the position a return equal to the financing cost embedded in the long position. In effect, this trading strategy is targeting the rates being paid in the equity repo market, which tend to fluctuate based on market conditions as well as whether the borrowing is short term or long term.

With the success of the Eurostoxx 50 total return futures, Eurex has expanded the range to include total return futures based on two other indices, one based on the banking sector and the other on companies with relatively high dividends. And most recently, it has introduced total return futures based on the FTSE 100, the main index for the UK stock market. The contract was launched in April 2021 and took off in 2022. As of April 2023, open interest stood at a little over 200,000 contracts with a notional value of £21 billion.

Understanding the repo rate implied in the pricing of total return futures

To help build interest in its total return futures, Eurex worked with market participants to explain the features of these products. One of the most important features is the equity financing rate that is incorporated into the pricing of these futures along with the performance of the index and the distribution of dividends. This rate reflects the income that banks and other dealers receive from lending shares to hedge funds and other investors. The following description of the equity financing rate comes from a discussion with an equity trading strategist at Citi that Eurex hosted in 2021.

When an asset manager buys a TRF from a dealer, the dealer hedges the trade by buying physical shares. They then lend these physical shares out to the market and extract an income from it, which is the repo rate. They pass this extra income to the buyer with a lower TRF spread—the higher the repo, the lower the TRF spread. However, while investors receive 100% of realized dividends, the dealer is taxed on physical shares, so there is a dividend mismatch. Dealers therefore pass through the dividend holding cost to the initial buyer via a higher TRF spread and therefore a higher TRF price. The equity financing rate or TRF spread the buyer pays is calculated based on minus repo, plus dividend tax times dividend yield.