Global commodity futures markets have a rich history. The earliest recorded example of an organized commodity futures exchange dates to around 1700, when Japanese merchants petitioned the shogun to authorize trade in rice futures at the Dojima Exchange. Some informal examples date even earlier, including operations of what is now the London Metal Exchange taking root in the 16th century via what was then called the Royal Exchange.

Modern commodity futures markets provide many of the same important functions, including price-discovery and risk-management. Here's everything you need to know about commodity futures trading and clearing:

What are commodity futures?

A commodity futures contract is a legal agreement to buy or sell a specific good at a predetermined price, and at a predetermined date in the future. There are commodity futures for energy products like oil and natural gas, agricultural goods like soybeans and corn, and metals like gold and steel. There are also environmental commodity markets including carbon futures that help put a price on emissions as part of the market-driven fight against climate change.

The commodity futures market is an important tool for the discovery of prices in key goods, as they inherently account for forward-looked expectations that the current price (or "spot" price) may not account for. They also provide a crucial risk-management service, allowing producers as well as end-users to lock in future prices to provide more certainty for their operations.

What does a futures exchange do in commodity markets?

Futures exchanges allow for efficient markets by supporting a central point for transactions, pooling the trading volume in one place.

Not only does this allow for efficiency of trading, as market participants can do business through a large central institution at scale rather than navigate a long list of individual buyers and sellers on their own; it also allows for efficient price discovery. The more buyers and sellers that there are doing business in one place, the more confidence market participants can have that they aren't missing a better price elsewhere.

What is clearing in commodity markets?

Clearing is part of a well-regulated process known as "settlement," where a commodity exchange helps guarantee a transaction between a buyer and a seller. In modern and interconnected global commodity markets, the system would break down if buyers and sellers can't trust that their counterparty will make good on their trades.

Specialized organizations known as central counterparties, or CCPs, act as the key intermediary between buyers and sellers to reconcile orders and stand behind futures contracts – even if the buyer or seller ultimately can't meet its financial commitments under the transaction. This factor ensures the orderly matching of all buy and sell orders.

What is a commodity futures broker?

In simplest terms, a broker is an intermediary who helps connect customers to commodity futures exchanges to transact. There are a number of services they provide in support of this role, including educating customers on the current array of products, placing timely trades, and helping manage delivery of physical commodities when appropriate.

Additionally, brokers support the clearing ecosystem by providing access CCPs and guaranteeing customers' trades at those CCPs. Doing so adds more resilience to the clearinghouse by mutualizing risk.

Brokers charge a fee for these services, but many customers would not be able to participate in global commodity markets without a skilled broker on their side.

How do other intermediaries support commodity markets?

Intermediaries in commodity markets are known by a host of names, including market makers or liquidity providers or even "speculators" by some. But whatever they are called, these firms play a foundational role in commodity futures trading because they help connect buyers and sellers across time.

Think of it this way: If you are a farmer and want to lock in the price of your crops by selling a huge lot of corn futures with a September delivery date, you have very few potential customers other than major food service or industrial companies. Conversely, if you're a major corporation that needs a huge lot of grain you could struggle to get a fair price if there aren't enough potential sellers on a given day.

This scenario is particularly true in certain "illiquid" markets without many buyers or sellers, such as the European Emission Trading Scheme (ETS) that involves carbon futures trading. On the EU ETS, there is generally only one supplier of emission allowances via the government, and market participants looking to manage carbon price risk need intermediaries to support efficient buying and selling.

Simply put, if there are intermediaries who are willing to provide regular liquidity to global commodity futures markets, everyone can execute trades faster and at a better price.

How are commodity futures markets regulated?

Though the overseeing bodies differ by geography, commodity futures markets are highly regulated in all corners of the world. In the EU, commodity futures markets are subject to a comprehensive set of rules following from EU financial regulation, including MiFIR and EMIR. In the US, the markets operate within a regulatory framework established by the Commodity Exchange Act and overseen by the US Commodity Futures Trading Commission. And in early 2022, China passed a historic Futures and Derivatives Law to govern derivatives trading and to facilitate internationalization of key commodity futures markets.

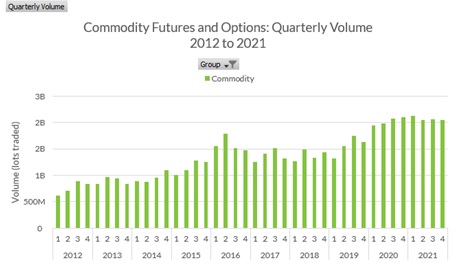

How big are global commodity futures markets?

While trading activity varies at times based to market conditions, global commodity derivatives trade several billion contracts each year. Some of the most popular commodity futures are tied to crude oil, soybean or steel products.

Data for key commodity derivatives activity from 2021 is below.

|

Category |

Jan-Dec 2021 |

Jan-Dec 2020 |

Volume |

2021 December |

2020 December |

Open Interest |

|

Agriculture |

2,820,109,552 |

2,570,657,307 |

9.70% |

23,622,214 |

22,988,649 |

2.80% |

|

Metals |

2,765,534,503 |

2,398,531,605 |

15.30% |

15,227,172 |

14,268,665 |

6.70% |

|

Energy |

2,710,751,767 |

3,151,107,672 |

-14.00% |

61,400,612 |

61,463,956 |

-0.10% |