We often talk about oil being a global market. But what does that mean? We found out on February 28 when the US and Israel first bombed Iran. All of us quickly learned how disruptions in a narrow waterway in the Mideast could cripple energy markets around the world.

I saw how dramatically the markets responded when ships could no longer move freely in and out of the Strait of Hormuz. Prices jumped for all sorts of commodities beyond oil, including fertilizer, aluminum, methanol, sulfur and helium. And the impacts have rippled through the global supply chains for a host of industries.

Such moments remind us that hedging and price discovery have always crossed borders — and that the institutions and regulatory frameworks must be equally mindful of our interconnected world.

Long before globalization became a common phrase, the futures markets had been international. Take agriculture as an example. A bumper crop in Brazil depresses prices in the US, and vice versa, so farmers in both regions need access to a futures market that accurately measures supply and demand at the global level.

Today, global interconnectedness is one of the defining strengths of our industry. Buyers and sellers from every region can participate in deep and liquid markets that provide price discovery and risk management on a scale that no individual country could replicate on its own.

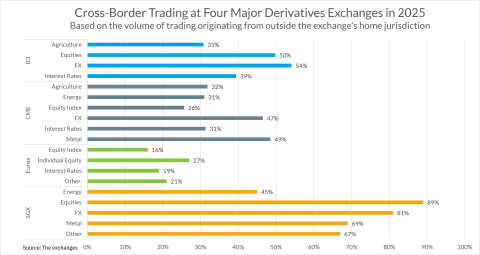

We see this in the data. We asked four global futures exchanges to provide us with data on the percentage of their trading volume that comes from outside their home jurisdiction and compiled it into the chart below.

The takeaway: all these exchanges benefit from cross-border trading. The exact ratio varies by asset class, and some exchanges are more geared to international flows than others. But the bottom line is that end-users who come to these exchanges benefit from a deeper pool of liquidity. And that liquidity leads to more efficient markets and more cost-effective hedging.

Our global regulatory environment must recognize this reality. When regulations overlap unnecessarily, conflict with one another or create duplicative requirements, market participants must deal with the resulting fragmentation. That fragmentation raises costs, reduces efficiencies and ultimately affects the end-users that rely on derivatives markets to manage risk.

That does not mean every country should have identical rules. Nor does it mean regulators should surrender their authority or compromise their responsibilities. National regulators rightly tailor their frameworks to the needs and characteristics of their own markets. But differences should not become barriers.

Cross-border markets function most effectively when the authorities respect one another's supervisory frameworks and focus on comparable regulatory outcomes. This principle of regulatory deference has served the derivatives markets well. It has allowed firms to operate across jurisdictions while ensuring that regulators retain robust oversight and accountability.

Ultimately, regulators have the same goals: protecting customers, promoting market integrity, reducing systemic risk and ensuring resilient market infrastructure. When they focus on outcomes, they create more space for markets to innovate and grow.

In an interconnected world, no regulator can effectively oversee global markets alone.

In the end, trust is the foundation of every market. And trust grows strongest when nations and regulators work together. Markets are strongest when they remain open, competitive and globally connected.