On 17 December, the Commodity Futures Trading Commission hosted a meeting of its Global Markets Advisory Committee to review the COVID-19 pandemic’s impact on derivatives clearing and to discuss regulatory developments in 2020 related to cross-border trading.

In her opening remarks, CFTC Commissioner Dawn Stump, sponsor of the GMAC, stated she was hopeful the meeting and its participants would "contribute to the ongoing dialogue regarding lessons learned from the [COVID-19 related] market volatility so global clearing systems can remain resilient in the face of future market stresses."

The GMAC is comprised of experts from banks, trading firms, exchanges and other stakeholders in the derivatives markets, and serves as a forum for the CFTC to gather feedback on market trends and regulatory issues. Although it has no formal rule-making powers, its findings often influence the CFTC's policy-making agenda.

Impact of COVID-19 global clearing and margin

FIA board chairman Nick Rustad, head of global clearing at J.P. Morgan, gave a data-driven presentation to the GMAC that showed the global cleared derivatives markets proved resilient amid the "real-world stress test" driven by pandemic-related disruptions in March and April. However, he also identified concerns about the procyclical nature of CCP margin.

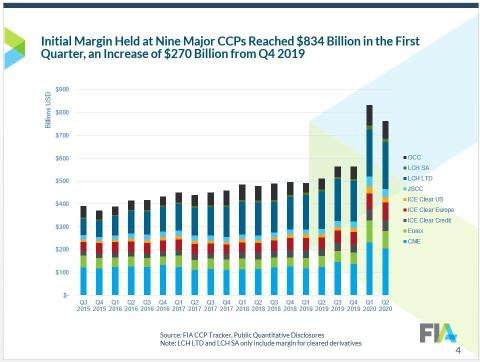

Specifically, Rustad shared FIA data that showed initial margin rose from $563 billion at the start of the first quarter to $833 billion at the end of the first quarter, and that margin breaches reported by clearinghouses in Q1 were more than the preceding 12 months combined.

Rustad said that "procyclicality [of initial margin requirements] contributed to overall market stress" and that "initial margin requirements created pressure on clearinghouse members and their clients and were sometimes not transparent, making them hard to predict in advance." He also offered several potential areas where clearinghouse margin requirements could be improved, including a review of margin floors, standardization of intraday margin calls to minimize ad hoc requests, and improvements to margin models to dampen procyclical effects. These recommendations echo FIA’s recent whitepaper on the impact of pandemic-related volatility on CCP margin requirements.

Rustad also presented data from his firm's internal analysis showing that the margin requirements for interest rate swaps were much less procyclical than the margin requirements for comparable interest rate futures, and urged policymakers to reconsider the margin requirements based on the liquidity and nature of the product.

Sean Downey, executive director, clearing, risk & capital policy, CME Group, noted in his presentation that CME Clearing did not implement any new policies or procedures in managing volatility despite the historic nature of the market disruption. Downey stated the absolute size of the initial margin increases were relatively modest, particularly when compared to the market volatility experienced.

Dmitrij Senko, chief risk officer, Eurex Clearing AG, noted in his presentation that extreme market moves necessitated an extraordinary number and volume of intraday margin calls in March 2020. Senko acknowledged some of the concerns raised in FIA’s margin whitepaper, agreeing that a review of the margin floor recommendations would be appropriate moving forward.

Sayee Srinivasan, deputy director of the Risk Surveillance Branch at the CFTC’s Division of Clearing & Risk, offered up many statistics and charts exploring the data behind margin volatility and promised more analysis would be forthcoming throughout 2021 on the topic.

Examining global clearing regulatory developments

The GMAC meeting also featured a panel with representatives from the CFTC, the European Commission, and the Japan Financial Services Agency. The panel focused on regulatory developments affecting the global clearing system, including the recent introduction by European regulators of a new supervisory regime for non-EU clearinghouses. Patrick Pearson from the European Commission noted that there were no US CCPs that would be considered “systemic to the EU” under the new regime. Commissioner Stump noted that these presentations “highlight the importance of mutual recognition of comparable, comprehensive regulatory frameworks for supervising CCPs around the world.”

Panelists and GMAC members agreed it is important for regulators from jurisdictions around the globe to maintain an open dialogue and to work toward mutually beneficial outcomes that strengthen the global clearing ecosystem and protect market participants.

Official statements and documents

- Statement of Commissioner Dawn D. Stump Before Global Markets Advisory Committee Meeting

- CFTC presentation: Registration with Alternative Compliance for Non-U.S. Derivatives Clearing Organizations

- FIA presentation: March Volatility and Clearing

- CME presentation: CME Clearing’s Margining Practices: CoVidPandemic

- Eurex presentation: Eurex Clearing margin performance during 2020 and reflection on the industry discussion

- CFTC presentation: Cleared Derivatives –March-April 2020 and beyond