At the end of 2019, FIA and market intelligence and advisory firm Greenwich Associates conducted an in-depth analysis of trends in derivatives clearing and plot key trends for the future.

Responses came from every corner of derivatives markets—from asset managers to brokers, from exchanges to clearing members, from traders to compliance officers. Their answers, reflecting the views of nearly 200 market participants, paint an interesting picture for the industry as a whole and offer detailed information into key segments and business lines.

One area of the FIA-Greenwich research that proved particularly interesting pertains to customer behaviors and expectations. Based on the research results, here is what end-users think about the state of the derivatives industry and where it could be headed in 2020 and beyond.

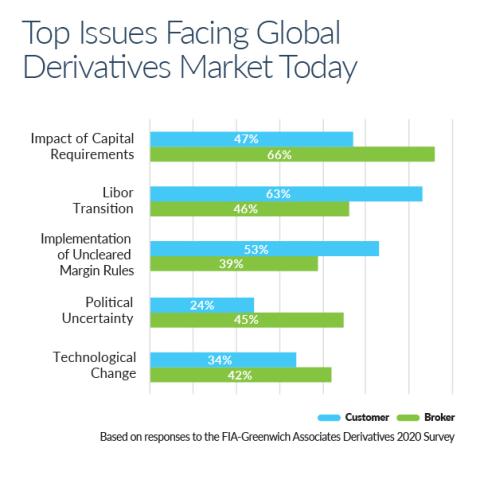

Top end-user concerns for 2020

The joint study offered several questions regarding the top issues facing global derivatives markets in 2020. And perhaps unsurprisingly, the challenges facing end-users differed materially from the concerns that are top-of-mind for brokers or clearinghouses.

For instance, while the No. 1 issue industry-wide was reported as the impact of capital requirements, a closer look at the breakdown of respondents shows that buyside market participants were not as concerned; though 61% of all respondents highlighted this as a key concern, only 47% of end-users responded that it was a top issue.

In contrast, the transition away from Libor was the top issue for end-users, with 63% of end-users pointing to this as a top concern. That compares with only about 46% of brokers, clearers and vendors naming the Libor transition as a top issue.

This assuredly reflects uncertainty among this core group of market participants as to how to proceed with this effort, which is unprecedented in both the scope and scale of the switch. While regulators and industry groups have been vocal in their support of alternatives including the Secure Overnight Financing Rate (SOFR) in the U.S. and the Reformed Sterling Overnight Index Average (Sonia) in the U.K., it is ultimately end-users that shoulder the burdens of that switch. This includes the real risk of a "haircut" after the hundreds of trillions of dollars in financial instruments tied to Libor are instead benchmarked to one of these new rates, as well as the practical challenge of managing fallback language, aligning hedges during the transition, and deploying new technological infrastructure to accommodate this new environment.

That challenge is daunting, as reflected by the fact that a mere 21% of end-users report they are "appropriately prepared" for the transition, compared with an overall response of 41% across the derivatives industry. But even worse is the fact that 9% of buyside respondents warned that they have not even begun working on a plan because of resource constraints.

Another area where end-user concerns diverged from the industry-wide average is in regards to the implementation of uncleared margin rules (UMR) for initial margin. Though the first phase of UMR began with a phase-in for the largest market participants back in 2016, the final phase-in periods through 2021 have many market participants concerned about potential disruption to uncleared derivatives markets. Phase 5 and Phase 6 of UMR will extend initial margin requirements to hundreds of smaller asset managers, straining their legal and operational resources.

Responses to the FIA-Greenwich research indicate the latter phaseins come with some headaches. The survey responses also likely reflect the fact that surely some market participants are hoping to avoid the formal oversight of UMR but still face very real concerns such as obtaining compression services or moving positions into futures markets to reduce the notional value of derivatives portfolios below the $50 billion UMR threshold.

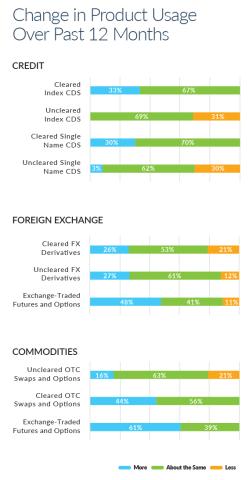

Product usage trends

As a group, the end-users who responded are active across many types of derivatives. When asked which asset classes made up the primary focus of their derivatives trading, respondents chose rates (67% of responses), equities (64%), commodities (56%) and foreign exchange (53%) all in significant measure.

When asked to list the purposes of their derivatives trading, the top choice was hedging market risk (57%), followed by implementing an investment strategy (51%). These more tactical uses of derivatives both ranked higher than increasing investment returns (40%), hinting that modern derivatives markets provide an efficient way to manage market risk exposures.

Looking forward, the research report indicates that end-users are increasingly gravitating towards cleared products. When asked about their credit product usage over the last 12 months, more than 30% of respondents said they were using less of both uncleared index credit default swaps (CDS) and uncleared single-name CDS contracts. At the same time, respondents said they used cleared index and single- name CDS derivatives more often or at a similar rate to the prior year.

Responses showed a similar movement towards cleared products in the commodities space, too, with 21% of respondents reporting they used less uncleared OTC swaps and options in the last 12 months — but not a single respondent indicating reduced use of either cleared OTC swaps and options, or in their use of exchange-traded futures and options.

In summary, the research indicates that the majority of end-users are engaged in derivatives markets to hedge or engage in other strategic investment goals beyond simply profit-seeking. And perhaps because of this focus on risk management and hedging, it is natural for these customers to gravitate towards cleared markets where a central counterparty helps provide greater transparency and certainty in a trade.

Clearing firm relationships

With this gravitation towards clearing, it is interesting to also explore how clearing firm relationships are measured by end-users. The FIA-Greenwich survey asked respondents to rank key quality measures for clearing firm relationships, and the top two factors were the quality of operational processes (64%) and fees (61%).

Clearinghouses will perhaps be pleased to learn, however, that the research indicates that they are meeting these needs quite well; 58% of respondents said they had not terminated a clearing relationship within the last five years, and 74% said their "most recent" relationship with a new clearinghouse is at a least two years old.