Please note that this is a working document provided by Eurex and may be updated periodically. Updates will receive new version numbers and the changes will be outlined.

Version 3.0 (25 January 2023). Changes made to reflect changes to timeline.

Q&A Table of Contents

What is the NextGen initiative?

Why is Eurex making these changes and improvements?

What do clients need to consider?

2023 migration plan and product code changes during integration period

Introduction

The following Q&A aims to provide a standardised set of high-level information, regarding Eurex’ s Next Generation Exchange Traded Derivatives (ETD) project to aid execution broker and clearing firms' communication to end clients, and particularly clients who use multiple clearing firms. This Q&A is not intended to cover all possible Next Generation ETD readiness issues and clients are advised to discuss any concerns or issues directly with your FCM(s) via your relationship manager or client services representative.

*Disclaimer*:

This document has been produced in cooperation with Eurex Clearing for informational purposes only and is provided for the benefit of FIA members and its clients that execute on the Eurex Exchange and clear on Eurex Clearing. The content of this document has been provided by Eurex and is sourced directly from Eurex’s website. FIA has not checked the accuracy of the content of the document as of the date of publication. While we may keep the content of this document updated, we make no representation to update it following the date of publication.

This document is not intended to constitute legal or regulatory advice. FIA specifically disclaims any legal responsibility for any errors or omissions and disclaims any liability for losses or damages incurred through the use of the information herein.

Interested market participants are encouraged to reach out directly to Eurex in case of any questions in relation to the content of this document.

Who will be impacted?

Everyone who executes or clears on Eurex will be directly or indirectly impacted including:

- Clients of FCMs

- NCMs

- ALL clearing and / or execution only clients

What is the NextGen initiative?

The implementation of next generation ETD contracts aims to introduce a more flexible set-up of ETD contracts. The new concept enhances contract identification and allows for more than one expiration per month on a product level (sub-monthly contracts). The NextGen initiative impacts trading, clearing and risk management layers and breaks up the current YYYYMM identification logic.

The main goal is to have a YYYYMMDD contract identification in place creating the basis for new business initiatives. For example, this will mean that from 27 March the current format will change as follows (example provided for index options on DAX with product symbol ODAX):

Relevant fields for contract identification

** Only filled if contract frequency = Mo(nth).

(Note: If the preceding image on contract identification is difficult to view on your device, please click here for a PDF version)

The following three business initiatives will be the first to be launched using the new logic:

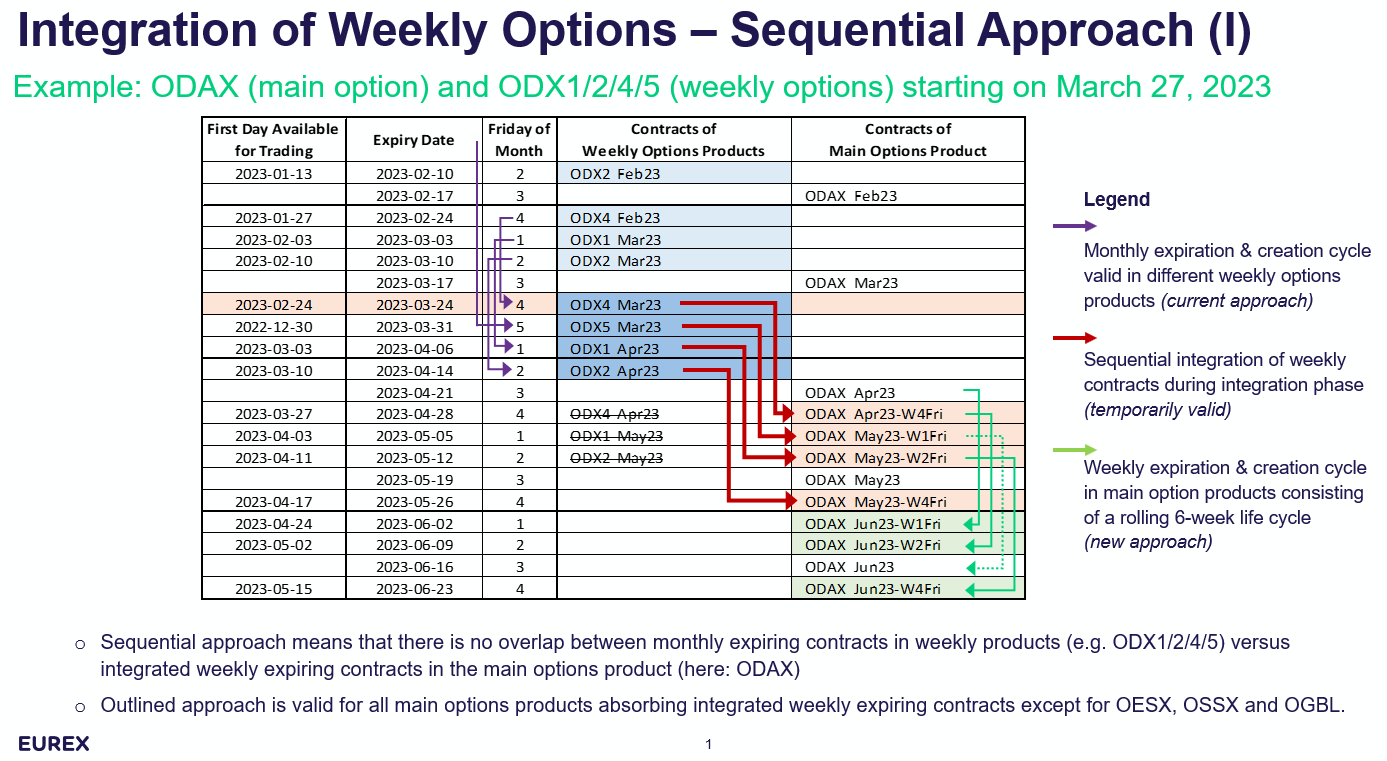

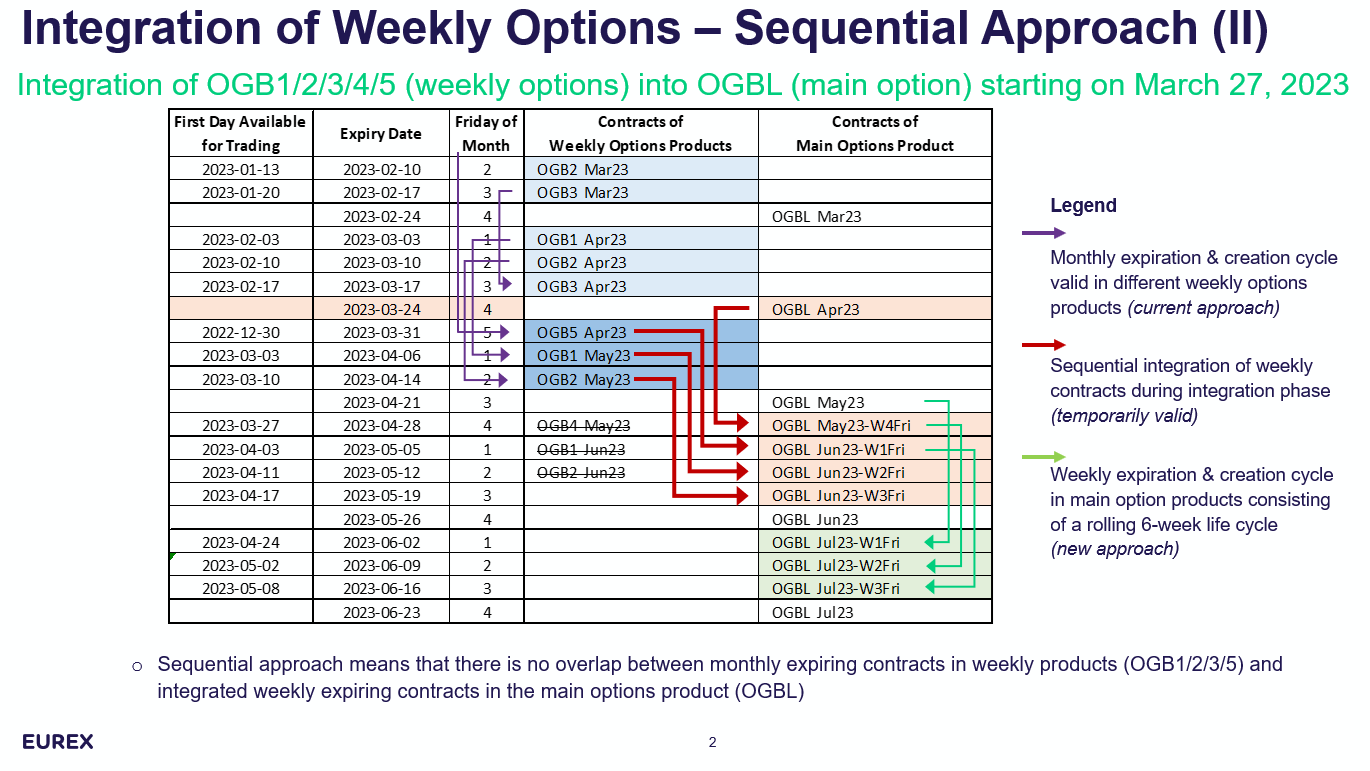

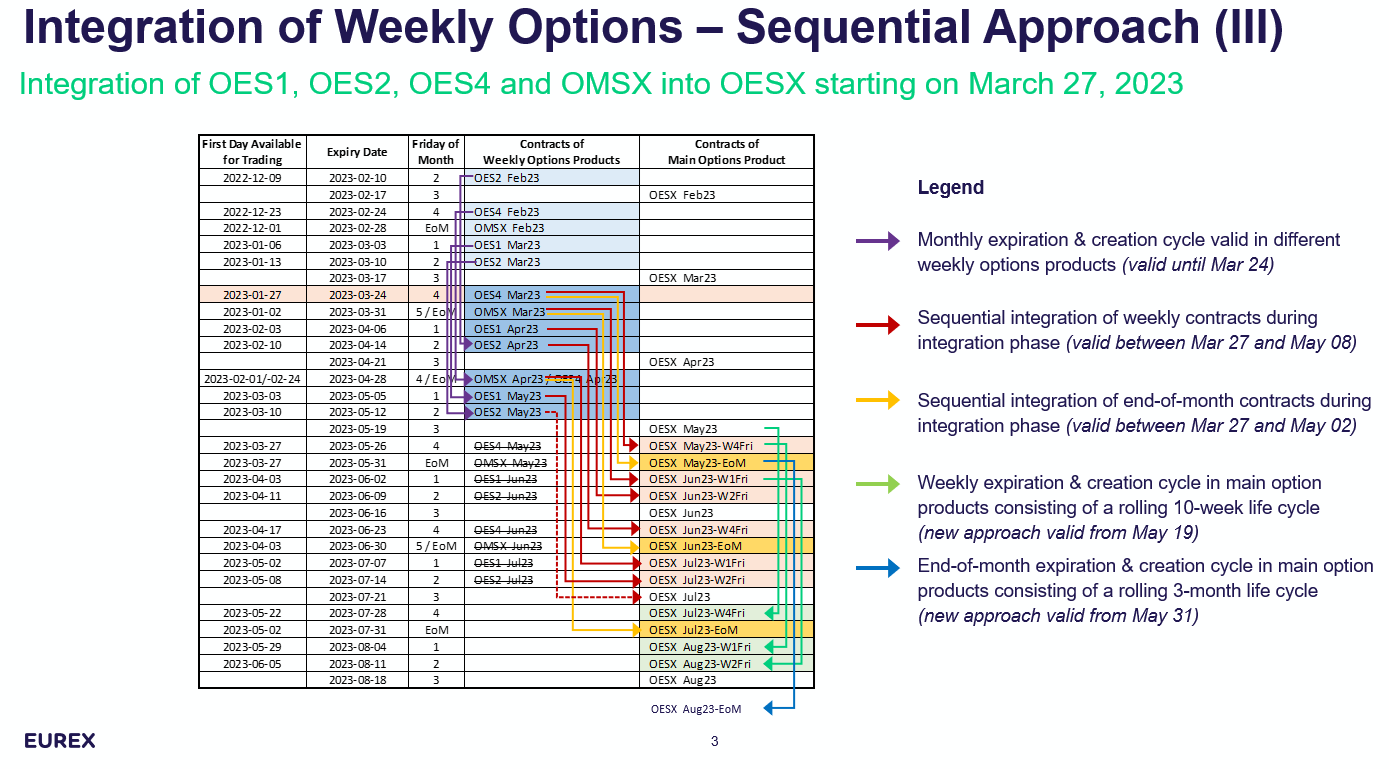

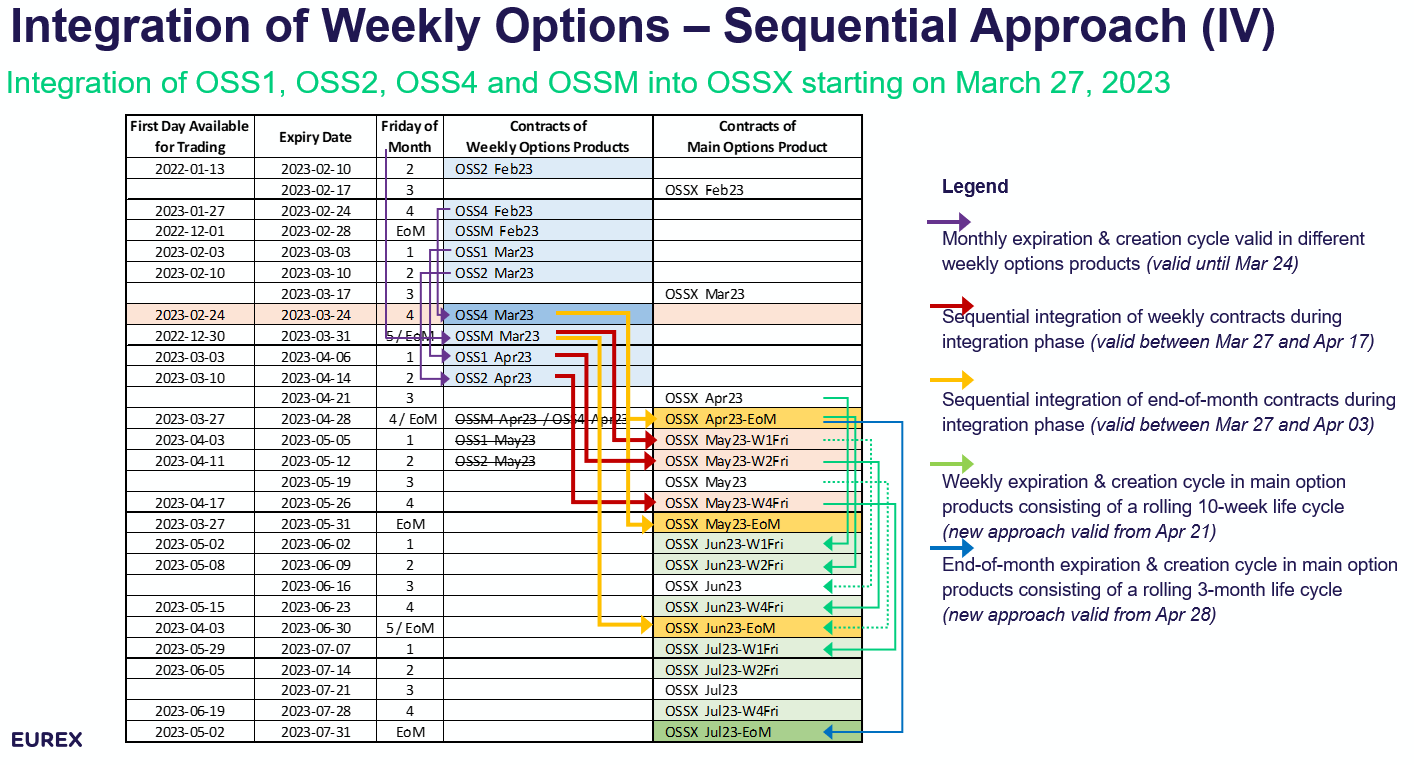

1. Integration of Weekly Contracts and End-of-Month Contracts

Monthly expiring contracts belonging to weekly options products will be integrated into the corresponding main options product as integrated weekly expiring contracts. This will affect all weekly options products in the fixed income, equity and equity index area including the options on the underlying EURO STOXX index (OESX) but excluding the KRX weekly options products OKW1, OKW3, OKW4, and OKW5. After the integration is completed, the weekly options products will become obsolete. Weekly expiring options contracts can also be used as leg instruments in any standard options strategy, non-standard options strategy and options volatility strategy. As an example, call or put time spreads as standard options strategy can be used to roll positions between weekly expirations or from weekly to monthly expirations in one transaction.

A similar approach applies to end-of-month contracts of options on EuroStoXX50 (OESX) and of options on EuroStoXX50 ESG (OSSX). As for weekly expiring options contracts, integrated end-of-month expiring contracts can be used together with monthly expiring options contracts as leg instruments in any options strategy.

(Note: If the preceding image on integration of weekly contracts is difficult to view, please click here for a PDF version.)

(Note: If the preceding image on integration of weekly contracts is difficult to view, please click here for a PDF version.)

(Note: If the preceding image on integration of weekly contracts is difficult to view, please click here for a PDF version.)

(Note: If the preceding image on integration of weekly contracts is difficult to view, please click here for a PDF version.)

2. Volatility strategies for Single Equity Options with daily expiring contracts in physically settled Single Stock Futures

Physically settled single stock futures will be equipped with daily expiring futures contracts having a lifetime of one business day. Consequently, on each business day, a new single stock futures contract will be created with individual T7 instrument ID and ISIN and will be expiring on the same business day. Daily expiring single stock futures contracts are used as leg instrument of an options volatility strategy of the corresponding options product allowing delta-neutral hedging in the stock options area with physical stocks.

3. Basis trading for MSCI Futures (Market-on-close) with daily expiring contracts in MSCI Futures

MSCI index futures will be equipped with daily expiring futures contracts having a lifetime of three business days. Consequently, on each business day, each MSCI futures product will have three daily expiring futures contracts available for trading, one contract with last trading day of today (T+0), a second contract with last trading day on the next business day (T+1) and a third contract with last trading day on the next but one business day (T+2). Daily expiring MSCI futures contracts can be used as the first leg in calendar spreads together with a quarterly expiring futures contract as second leg. Such a calendar spread is representing the basis instrument of the quarterly expiring futures contract and, consequently, will be denoted as “basis spreads”. On the expiration day of the daily expiring leg contract, the settlement price of the quarterly expiring leg contract will be identical to the underlying closing price plus the trade price of the basis spread.

Further information on the above is available from Eurex’ s website here.

These three business initiatives are being launched to attach the new flexibility in setting up ETD products with one big change.

Further initiatives will follow in due course.

Why is Eurex making these changes and improvements?

Eurex will introduce a more flexible set-up for ETD products to enable and cater for long-demanded trading strategies that can currently not be offered by Eurex. This is realized by implementing an enhanced contract identification concept that will be mandatory as of the 27 March, 2023, allowing more than one expiration per month on product level (sub-monthly contracts).

The introduction of the YYYYMMDD contract identification brings along the following new features, changes, and improvements:

- Integration of Weekly Expiring Instruments on Product Level

- Position rolling between weekly & non-weekly instruments by using standard options strategies

- Higher visibility of weekly expiring instruments

- Straight-through processing for volatility as well as basis trading

- Full CCP risk framework in place immediately after trade

- Implementation of daily expiring futures and calendar spreads

- Enhancements of clearing & settlement procedures

More information focusing on the trading aspects of the project can be found here.

More information focusing on the clearing aspects of the project can be found here.

When will changes occur?

Functional go-live: 27 March 2023

- YYYYMMDD logic becomes mandatory for all market participants for all ETD contracts.

- Simulation environments for T7, C7 and Prisma are up and running and provide ample testing opportunities for the new contract logic as well as sub-monthly expiring contracts.

Launch of NextGen business initiatives

- Integration of weekly expiring contacts starting as of 27 March 2023.

- Basis trading for MSCI Futures (Market-on-close) with daily expiring contracts in MSCI Futures on 24 April 2023.

- Volatility strategies for Single Equity Options with daily expiring contracts in physically settled Single Stock Futures on 17 April 2023.

What do clients need to consider?

The following list contains a non-exhaustive list of points clients need to be reviewed to assess potential impact. Please note:

- There may be internal mapping tables that may require updates.

- There may be bespoke touchpoints that clients should consider as well as other files or data feeds not listed here which may be impacted.

- It is recommended that all clients perform their own impact assessments.

Points for consideration include:

- Allocation files

- Exercise assignment

- Client reconciliations that need to change due to new YYYYMMDD contract identification logic

- Client's statements/ client RAW data files they receive from Clearing Members

- Clients need to inform that potential end clients

- System vendors/instrument vendors (It is recommended that clients contact vendors as there may be some work to undertake)

- Trade, Position and Cash files

- End of day or Intraday Pricing files

- Statements

- Exercise / Assignment instructions

- Closeout instructions

- Client reconciliations

- Confirmations

- Executions, including drop copies

- Margining files

- Any local mapping tables

- Any client specific flows related to their Clearing Members

Please note: There may be internal mapping tables that may require updates. There may also be bespoke touchpoints that clients should consider as well as other files or data feeds not listed here which may be impacted. It is therefore recommended that all clients perform their own impact assessments.

Vendor

There are several types of vendors that may perform more than one function / service which clients need to consider. These may include:

- Reference Data vendors (i.e., Bloomberg / Refinitiv / Euromoney Trade-data etc.)

- Any client who consumes any data direct from vendors, FCM’s or direct from Eurex should immediately contact their account managers to assess impacts and prepare for these changes as additional work may be necessary.

- Going forward Eurex will employ a combination of Symbol and Prompt Date to identify the correct expiration, clients (direct or indirect) and NCM’s should seek guidance from all their reference data providers for potential impacts.

- There may also be internal mapping tables which may require updates.

- Execution vendors (i.e., Bloomberg / TT / GLWin etc.)

- Back-office services vendors (i.e., FIS (GMI / UBIX) / ION etc.)

- Other data sources (i.e., pricing / margining etc.)

Client testing

Some clients may need to undertake several types of testing including:

- Directly with Eurex if you are an NCM.

- In conjunction with their FCM for any cleared activity.

- Clients may also need to test with their vendors depending upon the changes each client implements. (Even if no changes are confirmed by their vendors, it is recommended that clients perform regression testing).

Eurex simulation environment is supporting the YYYYMMDD contract identification logic and is listing sub-monthly contracts in the following products symbols.

- Integrated weekly expiring options contracts:

- Index Options: ODAX (including EoM contracts), OSMI, OESX (including EoM contracts)

- Stock Options: AXA, AFR, BAY, CSGN, ROG

- Options on Fixed Income Futures: OGBL

- Daily expiring MSCI futures

- FMWN

- FMWO

- FMEA

- FMJP

- Daily expiring Single Stock Futures supporting delta-neutral options volatility strategy trading

- AXAP

- BAYP

- BMWP

- ROGP

FIX tag information

The following fields and its tags are supported across the system landscape of Eurex, i.e. across trading, clearing and risk management system, and applies to all contracts supported by Eurex.

- Tag 541 – Maturity Date or Expiration Date with format YYYYMMDD

- Tag 30866 – Contract Date with format YYYYMMDD

Eurex recommends using tag 30866 – Contract Date since this field was explicitly introduced for the purpose of a unique contract identification on a day-month-year base. In most cases, the value of tag 30866 is identical to the value of tag 541. Currently known exceptions of this rule are MSCI options and futures contracts (where contract date and expiration date differ by one business day due to late closing price information regarding MSCI indices) and short-term interest rate futures contracts (where contract / expiration date is identical to the beginning / end of the accrued interest rate period which usually runs over 3 months).

For Eurex markets and for the time being, a one-to-one correspondence between tag 30866 and tag 541 applies which could also be used for a unique contract identification. However, the retention of this one-to-one correspondence is not guaranteed by Eurex and the one-to-one correspondence might not apply for other derivatives markets (e.g. energy derivatives market of EEX). Please note that a unique contract identification based on tag 541 does not work in case the one-to-one correspondence between tag 30866 and tag 541 is not supported.

Additional tags relevant for sub-monthly expiring contracts and supported across the system landscape of Eurex are summarized by the table “Relevant Fields for Contract Identification” depicted above in answer to Question 2 – “What”.

In case tag 200 – “Maturity Month Year” is used in combination with tag 205 – “Maturity Day” for contract identification, a translation toward tag 30866 or tag 541 is required to access the contracts supported by Eurex since tag 200 is not supported by Eurex for sub-monthly expiring contracts and tag 205 is not support by Eurex at all.

Please note that Eurex requested to take over the Eurex defined FIX tag 30866 into the FIX Standard Protocol 4.4. Detailed information will be provided at a later point in time.

Relevant fields for contract identification

** Only filled if contract frequency = Mo(nth).

(Note: If the preceding image on contract identification is difficult to view, please click here for a PDF version)