During recent market volatility caused by the Coronavirus outbreak, there have been questions raised regarding how exchange-traded futures and options could have negative prices. FIA has developed the following FAQ to help address these questions:

What is a futures contract?

Modern futures markets have been around since the mid-1800s to help farmers, producers and commercial businesses manage the risk of price fluctuations in commodities. Today, exchanges list futures on agricultural, energy and financial products. Futures are a standardized contract listed on a regulated exchange that obligates one party to buy or sell assets at a fixed price for delivery on a specific date in the future.

How do futures markets determine the price of a commodity?

Millions of these trades happen daily, allowing exchanges to centralize the prices of these transactions for a specific commodity, such as oil, corn, or interest rates. Futures markets aim to reflect the price in which supply and demand of a specific commodity come into equilibrium—known as a market clearing price. Prices of futures contracts fluctuate until buyers and sellers agree to a specific price. Dramatic changes in supply and demand can cause enormous volatility in prices as markets look for equilibrium.

It is also important to remember that the measure of a futures market's effectiveness is not if the futures price matches the spot price, which it rarely will in volatile and uncertain markets. Instead, it is how effectively it enables the convergence between the futures price and the spot price by the end of the delivery period.

Why is the price of oil futures so low?

The global oil markets are dealing with a large and growing imbalance between supply and demand. Demand for crude oil has collapsed amid a near total shutdown of economic activity in most parts of the global economy. Airplanes have been grounded, the roads are empty, businesses have closed, and factories are not burning fuel at the normal rate. On the supply side, oil companies have been scrambling to cut back on their production, but so far not enough to match the decrease in demand. This is what economists call "inelasticity," where the supply of a commodity cannot quickly adjust to meet changes in demand. This can lead to large price swings as the futures markets compensate for imbalances by reducing the price until supply comes back into line with demand.

This imbalance has been especially acute in the U.S. because it is both a producer and a consumer of oil. In recent years, the U.S. oil industry has increased production to such a degree that the country has become a net exporter of petroleum products. The sudden impact of the pandemic has reduced demand much faster than supply, and as a result, the tanks, pipelines and other infrastructure for storing the surplus oil are rapidly filling up.

Why did the price of oil futures fall below zero?

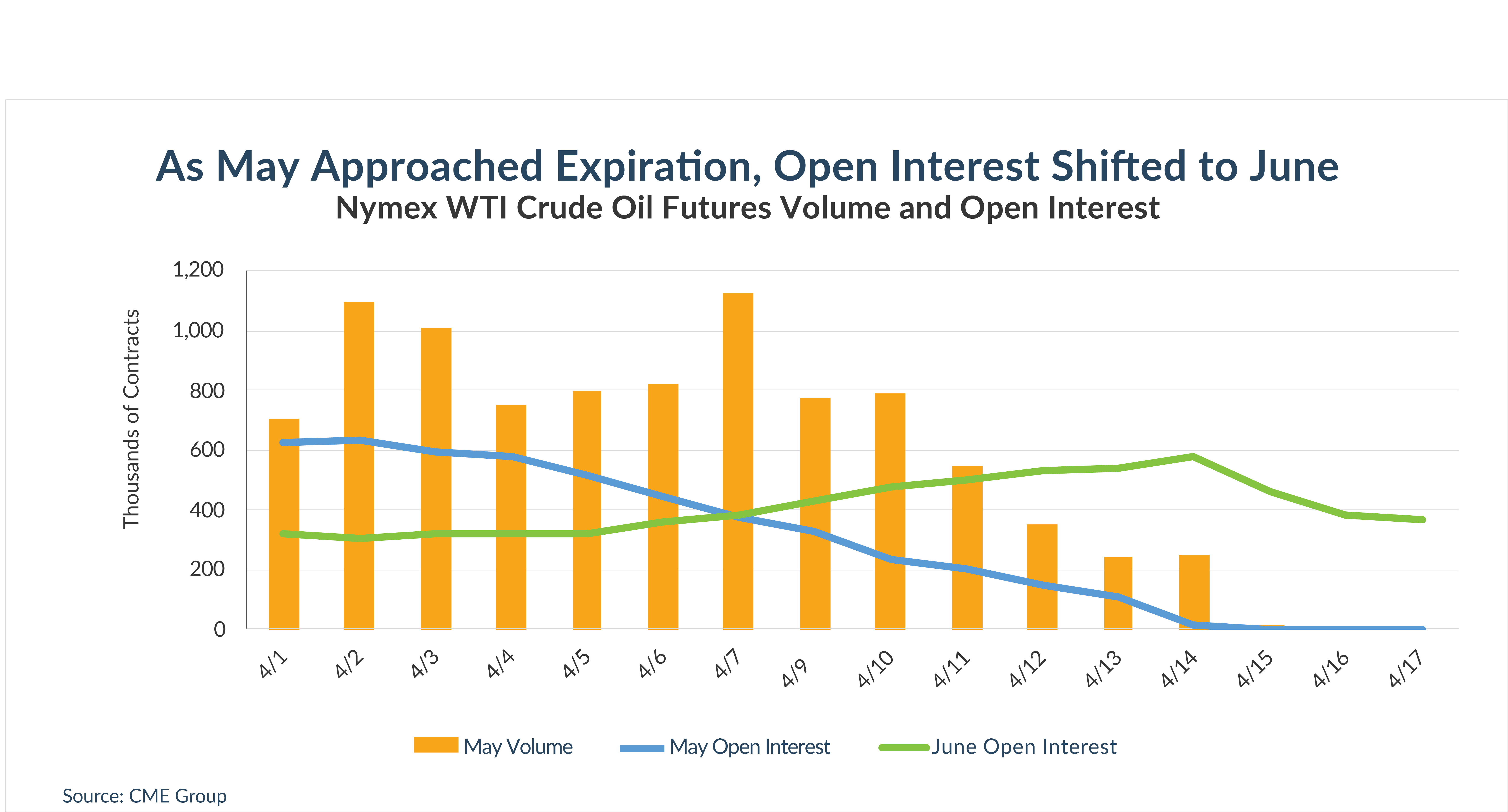

One of the global benchmarks for oil, the CME WTI oil futures contract, briefly fell below zero because of specific circumstances at that point in time. That futures contract is based on physical delivery of a specific quantity of oil at a specific location. When one of these futures contracts expires, the seller is obligated to deliver 1,000 barrels of light, sweet crude oil to the buyer, and those barrels of oil must be delivered at Cushing, Oklahoma, a central hub of pipelines and oil tanks.

As a result of the economic contraction driven by the pandemic, the supply of crude oil in the U.S. has risen so rapidly that it is overwhelming the available storage. According to S&P Global Platts, the storage tanks at Cushing were 75% full on April 17 and were headed towards 100% capacity by mid-May. In other words, the market was rapidly approaching the point where anyone buying barrels of oil through the futures market would have no place to store that oil.

Most traders anticipated this shortage of storage capacity at Cushing and closed out their positions well before the May contract expired on April 21. But some traders did not, and one day before expiration, they realized that they had to get out of their positions before expiration—or take delivery of barrels of physical oil with limited or no options for storage. This led to a wave of selling, and this is what caused the futures price to fall to a negative $37.63 per barrel on April 20 as the market looked for a clearing price.

The following day, the May WTI futures contract bounced back and settled at $10.01 per barrel, in line with the prevailing price for the same grade of physical oil in that part of the country. In other words, the futures converged with the physical at expiration, exactly as the markets are meant to do.

Has this happened before?

Yes, but rarely. There have been a few occasions in the past when the supply of certain types of petroleum products has exceeded demand to such a degree that producers were willing to pay buyers to take the excess supply off their hands. In addition, there have been occasions when the futures markets have posted negative prices for the spreads between different grades of oil, natural gas and other energy products. These instances of negative pricing were very temporary, and the markets quickly corrected.

Will it happen again?

That depends on whether supply of crude oil is reduced quickly enough to reduce the amount of oil in inventory. The June WTI contract is currently trading in positive territory, but oil continues to flow into Cushing and traders are watching inventory levels very closely.

Is the futures market broken?

No. The fact that a futures contract has a negative price does not mean the market is not functioning correctly. To the contrary, when supply and demand are that far out of equilibrium, the futures market would not be functioning correctly if it did not show a negative price.

Negative prices do create challenges for market participants, however. For example, trading systems need to be checked to make sure they can accommodate negative prices, and risk measurement methodologies may need to be adjusted to calculate the right margin requirements. For this reason, it is important for all market participants to understand that negative prices can exist and prepare accordingly.